After a second consecutive year in which the word “unprecedented” did more than its fair share of narrative heavy lifting, economists are looking ahead to 2022 with a sense of wariness: Sharply escalating prices and the uncertain severity of the omicron variant of the coronavirus cast twin shadows over forecasters’ expectations, but some still found reason for optimism in the face of such unknowns.

“2022 is what I’m going to call a transition towards normalcy,” said Eric Diton, the president and managing director of The Wealth Alliance, an investment advisory firm. “It means the global economy is going to continue to grow but not nearly at the rates that we saw in 2021. It means that inflation will still be stubborn — but going into the latter part of 2022, I think we’re going to solve a lot of those supply chain and employment issues,” he said.

Here are the top issues economists have on their radar for 2022:

The pandemic

The fast-moving omicron variant is proving to be the biggest near-term wild card. “The early part of 2022 likely will see another temporary slowdown in economic growth as rocketing omicron cases hit the discretionary services sector,” Ian Shepherdson, the chief economist for Pantheon Macroeconomics, said in a recent research note.

Early indications have suggested less-deadly outcomes, leaving forecasters cautiously optimistic, said Liz Young, the chief investment officer at SoFi. The U.S. is better positioned now than it was a year ago or even when the delta variant triggered a surge in caseloads in the summer and the early fall, she said.

“The health care system at this point is pretty well prepared to pivot and create different forms of vaccines and different forms of therapeutics as new variants present themselves,” Young said. As a result, stretches of market volatility that have accompanied each new variant and subsequent surge had become more muted, she said. “Those reactions keep getting shorter and shorter,” she said.

Experts acknowledged, however, that an epidemiological turn for the worse could upend the widely held view in markets that successive Covid waves will continue to have smaller impacts on the economy.

The housing market

According to data from the National Association of Realtors, the median price for an existing home rose to just under $354,000 as of November (the most recent month for which data are available), an annual increase of around 14 percent. Economists predict that the prospect of higher interest rates could act as a brake on home price gains next year because paying more to service mortgages leaves homebuyers with less money for payments each month.

Higher interest rates could act as a brake on future home price gains in 2022.

Daryl Fairweather, the chief economist of the online real estate platform Redfin, said in a new report that real estate activity will spike in the first half of the year as buyers and sellers alike scramble to close deals before rates rise. She predicted that 30-year mortgage rates will rise from their current level of about 3 percent to 3.6 percent by the end of next year, which would translate into an additional $100 a month at the median. Despite the rate pressure, however, Fairweather predicted that home prices will tick up by just 3 percent next year.

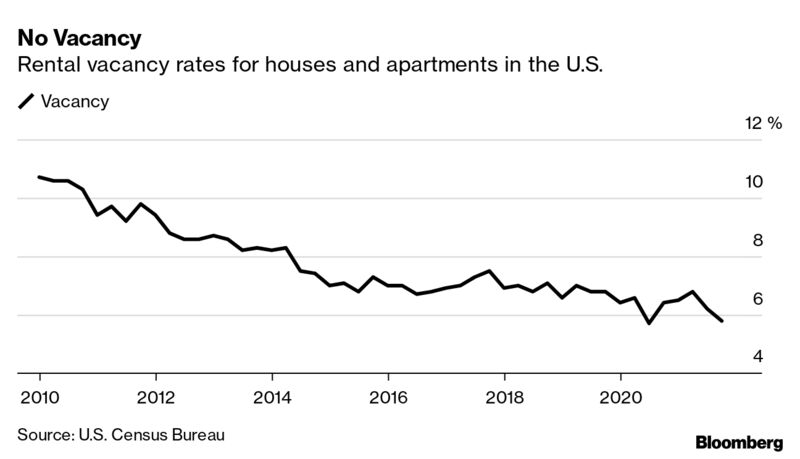

But while home prices might be cooling, renters aren’t going to get any kind of relief yet. “Rents are increasing at double digits,” said Jay Hatfield, the founder and CEO of Infrastructure Capital Management.

If the government still calculated inflation today using the same models it used back in the 1970s, the spike in rent costs this year would have been reflected in a real inflation rate north of 10 percent — a big reason the current inflationary climate has created greater financial challenges for renters. “This has basically never happened before. We’ve never had this kind of national inflation for rent,” Hatfield said.

Fairweather predicted another year of higher rents, estimating a 7 percent increase nationwide in 2022. “Demand for rentals will be strong for several reasons,” she said. “The end of mortgage forbearance will cause many homeowners to sell and rent instead. As the pandemic subsides, more people will choose to live in cities where it is more common to rent.” In addition, she said, the booming labor market and the ability of many knowledge-economy workers to do their jobs remotely could also trigger demand for rentals if newly arriving residents want to rent before they buy homes.

The supply of homes will remain an issue, economists say. A report in June commissioned by the National Association of Realtors found that the U.S. housing market has a demand-supply gap of 6.8 million units and that higher prices for materials and labor will make closing the gap even more challenging.

The stock market

Despite bouts of volatility, 2021 was a gangbusters year for stocks, with equities notching record highs regularly. With the gains all but in the rearview mirror, however, market professionals predict a return to sobriety next year.

“In 2022 we’re going to be looking at the fundamentals of it much more closely,” Young said.

A big open question is whether, when, and to what extent the services sector — which comprises a sizable slice of economic output and jobs — will be able to rebound. “If the services sector has come back ... I think the worst of the reaction is already behind us,” she said.

John Cunnison, the chief investment officer at Baker Boyer Bank, said, “If we start looking forward ... what seems to be priced into the stock market is just a massive amount of demand for financial assets.”

Cunnison pushed back against the assumption that a run-up in asset prices would necessarily trigger a hard landing. “This is not a dichotomous outcome,” he said. “You can grow into high prices. Earnings can continue to grow solidly into the current prices.”

If 2021 was marked by hope for the future, however, experts say investors will use corporate earnings as a window to look into the health of the U.S. consumer and, by extension, the country’s economic growth.

“What we’re watching for is the relative performance between the consumer discretionary sector and the consumer staples sector,” said David Wagner, a portfolio manager, and analyst at Aptus Capital Advisors. A reduction in nonessential spending could mean high prices start to pinch consumer spending, which could portend coming economic pain that could spill over into other categories of spending, squeezing earnings and triggering a downturn on Wall Street.

The labor market

It would not be an exaggeration to label 2021 as the year of the worker, and experts said the new year is likely to reflect more of the same — at least at first. “Longer term, I think we’re going to continue to see labor shortages ... but in the next year or so it’s going to get better,” Wagner said.

The consulting firm Deloitte found in a recent survey of chief financial officers that companies expect to invest in and spend on equipment, technology, and human capital next year. “There’s going to continue to be a significant increase in domestic hiring and domestic wages,” said Steve Gallucci, the leader of Deloitte’s chief financial officer program in North America.

Early retirement has moved more than a million workers out of the labor pool.

Yet even Federal Reserve Board Chairman Jerome Powell admitted that policymakers were perplexed by the extent to which labor force participation remained depressed this year. In the new year, experts say, the U.S. workforce will come closer to its pre-pandemic norm, but only up to a certain point. Some of the changes triggered by Covid-19 are likely to be, if not permanent, long-term fixtures of the labor market.

“I think that labor force participation stays below where it was before the pandemic,” Young said.

Early retirement has moved, by many estimates, more than a million workers out of the labor pool. “We’re just not going to replace those people,” Young said. “That’s something that we’ll just need to expect.”

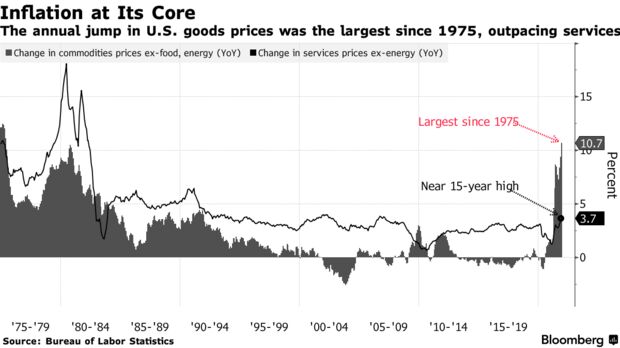

Inflation

The inflation question is paramount because it touches so many facets of the economic landscape: Federal Reserve policy and interest rates paid by borrowers, as well as prices on goods and services bought by individuals, as well as companies.

“I would argue what we’re seeing right now with inflation is a combination of two things. It’s a perfect storm,” said Brad McMillan, the chief investment officer for Commonwealth Financial Network. High demand for goods triggered by service-sector shutdowns and by supportive monetary and fiscal policy that was rolled out last year was on a collision course with a global supply chain that had effectively had sand poured into its gears.

One bright spot is the elevated rates of savings still held by many American families.

“All of a sudden, the demand for things spiked just as the supply of things cratered. The question going forward is is that going to continue?” McMillan said.

One bright spot is the elevated rates of accrued savings many U.S. families still hold. Bank data show that such reserves are dwindling, but some experts held out the hope that they could last long enough to buffer escalating inflationary pressures.

“I think the wild card here — and it gives Jerome Powell a little more flexibility — is the net worth of the U.S. household continues to get substantially larger,” Wagner said. Shepherdson, of Pantheon Macroeconomics, estimated that U.S. households will draw down $600 billion worth of savings next year.

Markets had been pricing in a trio of interest rate hikes in 2022 for much of the final quarter of 2021, which was reflected in the economic projections the members of the Fed’s policymaking committee made in December. The big unanswered question is whether that will be the right amount of tightening for an economy that has been anything but predictable over the last 22 months.