Multifamily's Complicated Supply Issue

The multifamily sector faces a complex supply challenge, with abundant ongoing development and varied implications across different locations and property types.

A Glut in Growth: Inside the Oversupply Problem in Multifamily Housing

The multifamily sector is experiencing a supply challenge, with an abundance of development in progress. However, this issue might not be as simplistic as it appears, with different implications based on location and property type.

Market segments: The impact of supply is not uniform, varying across low- to middle-income neighborhoods and wealthier suburban areas. Notably, affordable housing remains stable due to its long-term horizon and resilience against short-term market fluctuations. Rochelle Mills from Innovative Housing Opportunities indicates that public funds lend stability to this segment, with occupancy rates being consistently high.

Historical context: Jay Lybic of CoStar Group emphasizes that the current supply issue differs significantly from previous ones, particularly in terms of which market segments feel the impact. Unlike scenarios in the late 1990s, the present situation sees the “pain” of oversupply being mostly felt at the top end of the market, safeguarding the middle market to some extent due to a substantial price difference.

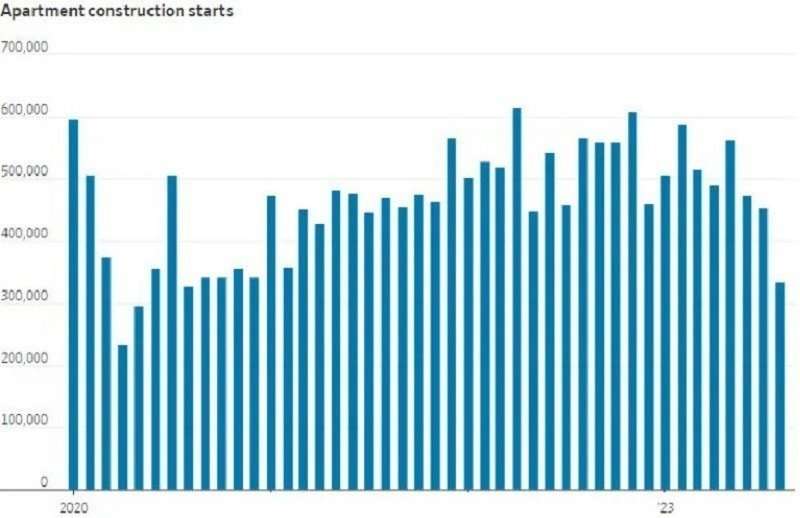

The demand: Despite high deliveries, long-term projections by institutions like the National Multifamily Housing Council estimate a requirement of 3.5 million new multifamily units over the next decade. Paul Fiorilla from Yardi Matrix notes that while the number of units under construction is substantial, rising rents — up 22% combined in 2021 and 2022 — indicate robust demand, as the market seeks to compensate for under-building following the global financial crisis.

Regional insights: The geographical aspect is pivotal in understanding supply and demand dynamics. While the Sunbelt is grappling with an oversupply, other areas, especially in the Midwest and Northeast, show stability or even a surge in their markets. The supply tends to be concentrated in rapidly growing markets like Austin and Phoenix, where population and job growth seek to balance the increasing housing units.

➥ THE TAKEAWAY

Big picture: Although oversupply poses short-term challenges, several experts predict the market will stabilize in the long run, as new units are gradually absorbed and demand stabilizes. Consequently, the forthcoming 12-18 months may be balanced as the market navigates through rent growth and stable investment options. Industry insiders like Jay Parsons suggest that a strategy centered around long-term views and patience will likely be rewarded, pointing to a potential equilibrium around 2025 when supply catches up.

Source: Multifamily’s Complicated Supply Issue

https://www.creconsult.net/market-trends/multifamilys-complicated-supply-issue/