eXp Commercial is one of the fastest-growing national commercial real estate brokerage firms. The Chicago Multifamily Brokerage Division focuses on listing and selling multifamily properties throughout the Chicago Area and Suburbs.

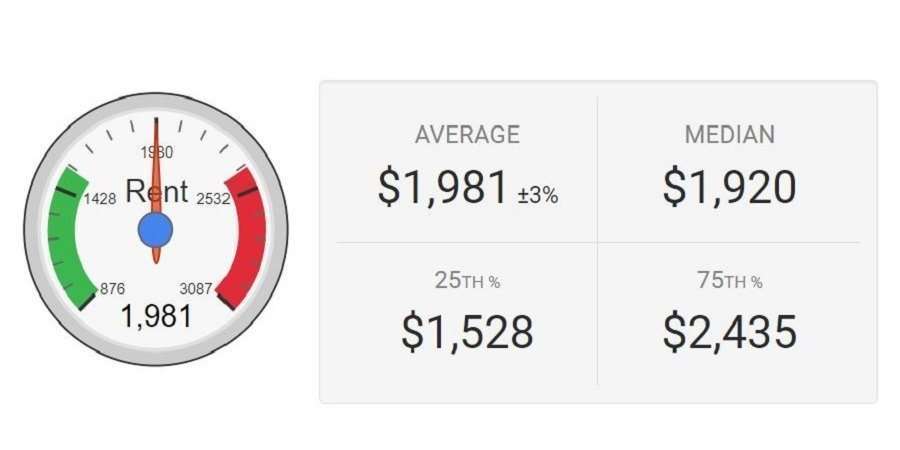

FREE Property Valuation What is my property worth? Be informed about the value of your multifamily property before you make a major decision. Request a valuation for your Chicago area multifamily property today. By providing current rent rolls and operating expense information, you will receive expert financial market and comparable sales analysis. Just one of the free resources offered to our clients to support their Multifamily Investments. https://www.creconsult.net/resources/

FREE Property Valuation What is my property worth? Be informed about the value of your multifamily property before you make a major decision. Request a valuation for your Chicago area multifamily property today. By providing current rent rolls and operating expense information, you will receive expert financial market and comparable sales analysis. Just one of the free resources offered to our clients to support their Multifamily Investments. https://www.creconsult.net/resources/

FREE Property Valuation What is my property worth? Be informed about the value of your multifamily property before you make a major decision. Request a valuation for your Chicago area multifamily property today. By providing current rent rolls and operating expense information, you will receive expert financial market and comparable sales analysis. Just one of the free resources offered to our clients to support their Multifamily Investments. Request Free Valuation: https://www.creconsult.net/resources/

FREE Multifamily Rent Analysis Request a free rent analysis for your multifamily property. With millions of rent comps maintained in the database, you can compare your rent with other local properties to be sure you are renewing and leasing at current market rents, optimizing your rental income and property value. Just one of the free resources offered to our clients to support their multifamily investments. https://www.creconsult.net/resources/

FREE Chicago Multifamily Market Report Download an in-depth market analysis report. REIS reports include historical rent and vacancy trends and other market fundamentals. Just one of the free resources offered to our clients to support their Multifamily Investments. https://www.creconsult.net/resources/

Apartment sales fell 17% in 2022, according to MSCI. Though the final numbers for 2023 haven’t been released, they will no doubt be lower than 2022’s figure after transaction volume dropped each month of the year.

At this point, the question on investors' and brokers’ minds isn’t if things will get back to the halcyon pre-interest rate hike days of 2021 and early 2022. Nobody expects that kind of market anytime soon. They simply want to know when the sales market will start to thaw out.

After the Federal Reserve's December announcement that it will likely trim the federal funds rate from the current range between 5.25% and 5.5% to 4.6% by the end of 2024, multifamily leaders could get their wish and see deals start flowing again this year.

“I don't know that [sales volume] can possibly decline any more than it did,” Kyle Draeger, senior managing director of multifamily debt and structured finance at CBRE Capital Markets, said. “My view is that it is not going to go down. I think it will get better.”

But even as sales improve, rate cuts won’t paper over all of the issues that emerged during the past two years, leaving some types of properties primed for sales. Here are four things buyers and sellers can look for in the coming year.

Sellers will come off the sidelines

Shortly after the Fed’s announcement, the 10-year Treasury, a basis for multifamily loans, dropped below 4.0%—a level it hadn’t hit since July—after hitting its highest level since 2007 in October.

Josh Bodin, senior vice president of securities trading with New York City-based commercial real estate services firm Berkadia, thinks lower Treasury yields should lead to more deal activity, which has been hampered due to interest rate volatility. “Once yields stabilize, investors should have more clarity on their cost of capital and pricing, which should lead to more sales and refinancing activity,” he said.

A major impediment to sales over the last 18 months has been pricing. As borrowing costs have moved, gaps have emerged between buyers and sellers on the price of assets. If rates come down, consensus should be easier to find.

“A stable interest rate environment will help lenders and investors become more closely aligned with the current state of capital markets, putting an end to the transaction halt that we have seen in the past months,” said Gerardo Mahuad, managing principal at Miami-based apartment owner and manager Eagle Property Capital, who recently closed a value-add fund.

With clarity on pricing, apartment owners who want to sell could come off the sidelines. “The once-motivated seller, who became sidelined due to the rate environment and the cap rate environment, is now suddenly motivated again,” said Marc Pollack, managing director for multifamily at Dania Beach, Florida-based property management firm FirstService Residential.

Forced sales won’t go away

However, some owners won’t have the luxury of waiting for values to recover. Rising borrowing costs have put pressure on owners with floating-rate mortgages. Plateauing rents and ballooning expenses will add to the problem.

“It's certainly an interest rate issue, but it's also a short-term operations issue as well,” said Spencer Gray, CEO of the Indianapolis-based apartment capital provider, owner, and operator of Gray Capital. “Higher operating expenses, especially some of the fixed costs, like insurance, property taxes, and payroll, are all up.”

The largest, best-capitalized owners will typically be in good positions, according to Gray. But others could face issues. “Even some good-sized middle market groups have multiple properties with bridge loans that are expiring soon or floating rate debt with interest rate caps that need to be repurchased,” he said.

Even if interest rates and the 10-year Treasury fall next year, these issues won’t magically disappear. There will still be some pain in the market, forcing buyers to take action.

“There will be forced activity, whether that’s recapitalizations, cash-in refinances, or sales,” Draeger said. “The Fed lowering rates will certainly help on the margin through interest rate cap pricing decreasing and lower coupons on permanent loans, but there will still be distress.”

More value-add properties will move

When properties do run into issues, it's usually because of their financing structure, not inherent issues in real estate.

However, Mahuad expects more value-added properties to be sold in 2024, as sellers are forced to transact. “It is more in the capital structures of sponsors that used very aggressive leverage to acquire properties,” he said.

A lot of buyers are also watching new deliveries in the supply-soaked Sun Belt markets. AvalonBay Communities is paying close attention to properties in lease-up that are facing nearer-term loan maturities, according to CEO Benjamin Schall on the Arlington, Virginia-based REIT’s third-quarter earnings call.

While Schall said equity and debt partners are currently working with developers, that could change. “There's going to be equity that doesn't have the ability to put in more capital, and it won't be the case for all types of lenders,” he said. “There's only certain profiles of lenders that can extend out. So, it's an area that we are staying close to.”

Some investors will want to exit

In some cases, equity may simply want to exit. According to executive chairman and co-CEO Stuart Miller on the Miami-based home builder's fourth-quarter earnings call, limited partners' desire to market the apartments drove Lennar's decision to market its roughly 11,000-unit rental housing portfolio. The company took a $25 million loss on the portfolio in the fourth quarter.

“The timing is one where it's kind of a suboptimal time to be thinking about a sale, although who knows where interest rates go?" Miller said. “That could change quickly.”

Miller is right. If there is one thing multifamily investors have learned since COVID-19 hit in 2020, it is that things change in a hurry. And that trend is likely to carry into 2024.

Apartment and Industrial Changed Course, Office Entered Uncharted Territory, and Retail in Holding Pattern

The year 2023 ended on a generally positive macroeconomic note: inflation has made solid progress, with year-over-year growth of the CPI (consumer price index) down as shelter receded to the same level in November 2019. The labor market dialed back its pace but remained steady. There are still 1.3 jobs per every unemployed person, higher than 1.2 pre-pandemic. The unemployment rate also fell to 3.7% in November, well below its long-run average. Real GDP growth stayed above the US's potential for most of the year and accelerated in the third quarter, attributed to consumer spending and inventory investment. The long-feared recession did not materialize, and the hawkish Federal Reserve subtly pivoted, hinting at the peak of the current rate hike cycle.

While the broader economy seems to be heading towards a soft landing, much of the commercial real estate (CRE) world is stuck in limbo. Why?

The multifamily and industrial sectors experienced sudden shifts in supply and demand dynamics

The office and multifamily sectors led the CRE market in value declines, characterized by a few high-profile fire sales

High interest rates compressed capital funding and elevated refinance risks

While many events were indeed idiosyncratic or metro-specific, others may well be part of regime changes or even leading indicators of a new equilibrium. Moody’s Analytics Q4 data shows where the core CRE sectors’ (multifamily, office, retail, and industrial) conditions stand as we conclude 2023.

Multifamily

Multifamily performance changed course in the fourth quarter, with net absorption plummeted from an average of over 45,000 units in the previous quarters to less than one fifth (or 8,973 units) nationwide, making Q4 another quarter with less than 10,000 units of net move-ins this year. Year-to-date, total net absorptions were only a third of their pre-pandemic highs, driven by the stabilization of demographics and the lock-in effect on the substitutional single-family housing market. While the journey to homeownership slowed, household formation was also challenged by a persistent rent burden especially on the lower end of the renter distribution.

Construction delivery over the investable space (20 units and above) fell short of initial estimates, with slightly over 40,000 units verified for the fourth quarter so far. According to the National Multifamily Housing Council’s quarterly construction survey, economic uncertainty, availability of construction financing, and economic feasibility are among the top reasons for project delays cited by the leading multifamily construction and development firms. We do expect upward revisions as we continue validating project completions over the next few weeks, but the glut of new supply significantly pressured the overall market performance.

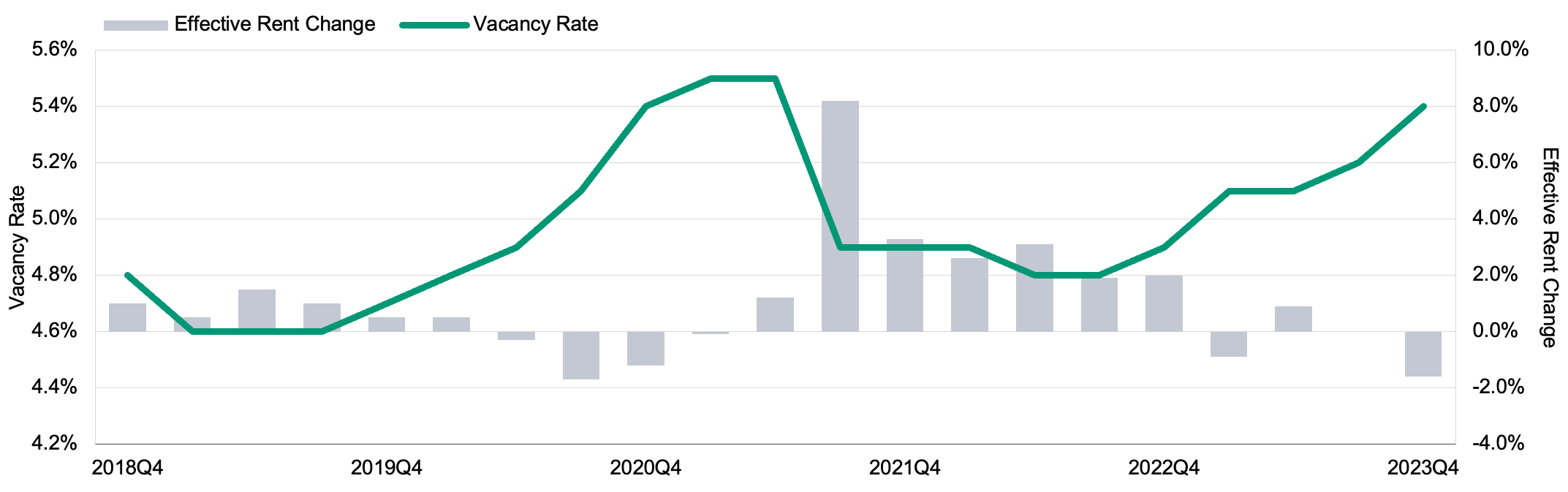

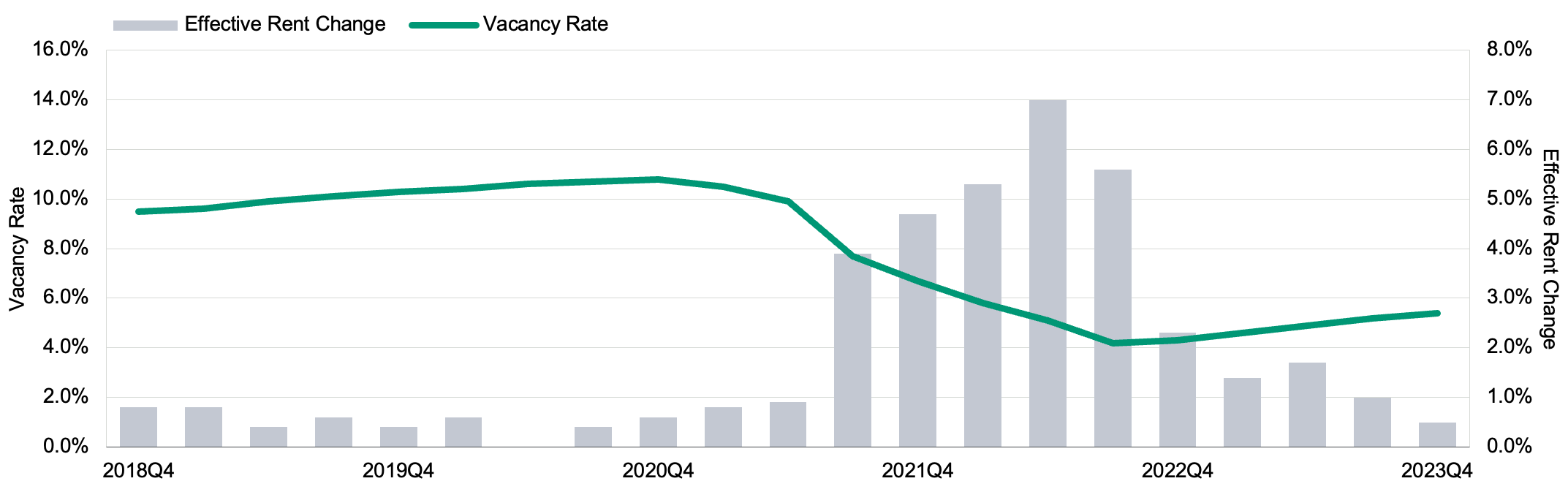

The national apartment vacancy rate went up 20 basis points (bps) to 5.4%, half a percentage point higher than last year’s and inching closer to its recent pandemic peak of 5.5%. A temporary imbalance of supply and demand compressed rent growth, with both asking and effective rent declining continuously in the last three months of the year. At the national level, asking rent was down to $1,825 while effective rent closed at $1,732, 0.8% and 1.7% lower than their respective year-ago levels. It is striking to see the widened gap between asking rent and effective rent, which grew at a record speed over the second half of the year from 4.1% to 5.1%, a level not seen since 2010.

Figure 1: Apartment Rent and Vacancy Trend: Effective Rents Declined as the Vacancy Rate Climbed in 2023

Moody's Analytics CRE

Office

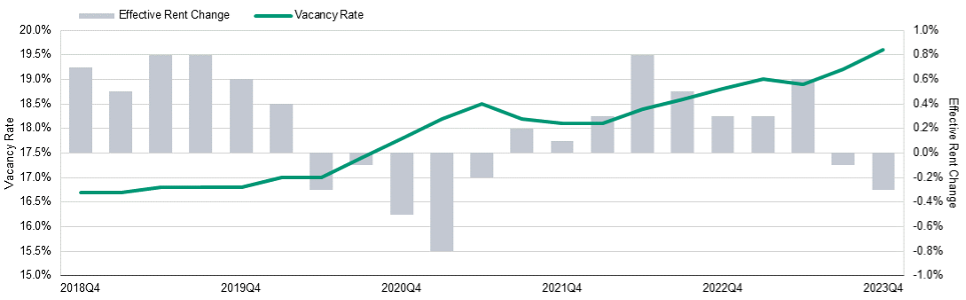

The national office vacancy rate rose 40 basis points to a record-breaking 19.6%, shattering the previous record of 19.3% set twice previously: once in 1986, driven by a five-year period of significant inventory expansion, and the other in 1991, during the Savings and Loans Crisis. This surge represented the largest quarterly increase since Q1 2021, setting the latest office vacancy 280 bps higher than its pre-pandemic level.

New construction has added 24,474,000 square feet (sqft) of office space since the beginning of the year, well below our initial estimate and the lowest since 2012. With annual inventory expansion currently sitting at 0.54%, new Class A properties that offer flexible or smaller configurations are particularly attractive to tenants who decide to keep the physical office footprint for branding, purposeful gathering, training, and collaboration purposes. Suburban offices also fared better due to their proximity to local communities and, in some cases, shorter commute times.

Despite the increasingly optimistic consensus on the likelihood of a soft macroeconomic landing along with positive news from the labor market, the permanence of dynamic hybrid models has effectively muted office demand, making the year 2023 the most downbeat since the Great Financial Crisis (GFC). Net absorption has stayed consistently negative since July 2023 and finished Q4 at -12,965,000 sq ft, driving the end-of-year total to -18,320,000 sq ft. Subleases also absorbed some level of office demand as the market continued to adapt to the regime changes. Asking rents rose by 0.1% in Q4, but effective rents declined for a second straight quarter by -0.3% due to considerably high vacancies.

Figure 2: Office Rent and Vacancy Trend: Historic Vacancy Levels Lead to Declines in Effective Rent in Q4

Moody's Analytics CRE

Retail

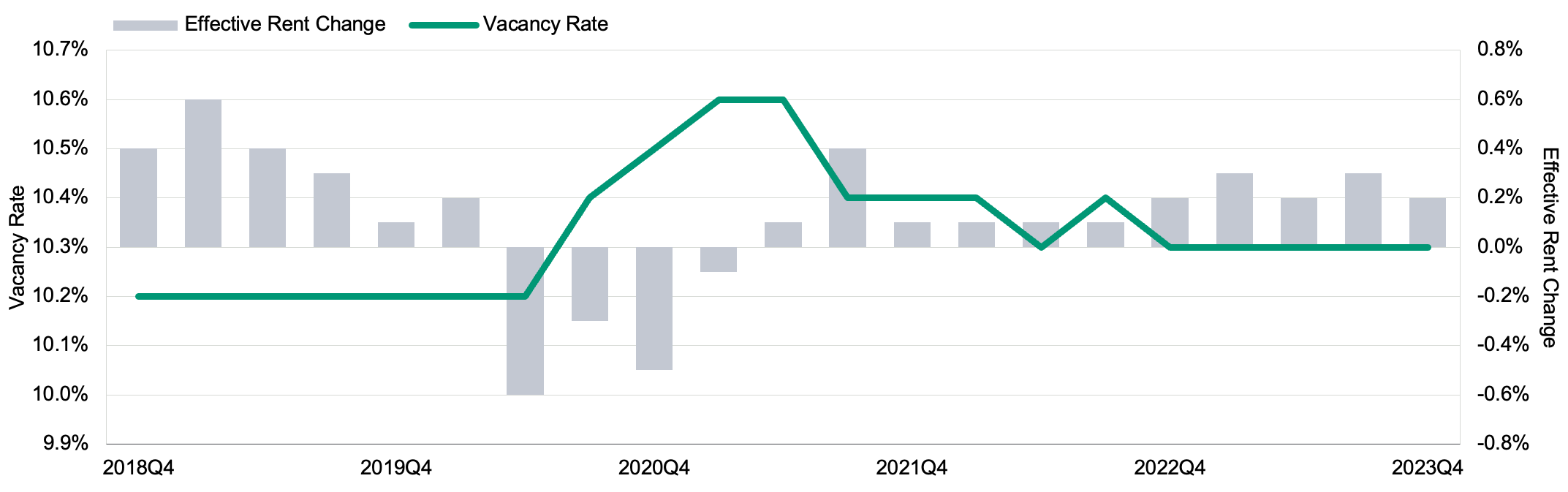

The retail sector remained largely steady throughout 2023, as the vacancy rate stayed flat at 10.3% in Q4. Asking rents rose by 0.2% to $21.7/sqft, while effective rents were up by 0.2% to $19/sqft in Q4. Early holiday season figures suggest consumers have continued spending, and retailers that have adopted omnichannel methods are in a better position to meet consumer needs by fusing in-person experiences with the ease and accessibility of online shopping. As consumers continue to subtly shift their preference from goods to services, physical experiences still have a place in the retail sector.

New retail construction grew by 583,000 sqft in Q4, bringing the preliminary year-end total to 5.7 million sqft, or 0.3% of inventory expansion. New construction faced many of the same financing and economic challenges as other sectors, but ongoing adjustment to a new equilibrium has lagged behind the consistent slowness in construction. While retail data indicates stagnation, a nuanced study shows persistent shuffling of winners vs. losers in the physical space. Elevated interest rates put many potential expansions, franchising opportunities, or even mergers and acquisitions on hold.

Bifurcated consumer spending habits challenged retailers that failed to adapt as the missing middle phenomenon persisted in 2023. Despite these significant headwinds, closer integration of live-work-play communities will save the retail form that used to heavily rely on commuting workers.

Figure 3: Retail Rent and Vacancy Trends: National Rent and vacant Levels Remained Mostly Flat as Retailers Navigated Uncertainty

Moody's Analytics CRE

Industrial (Warehouse/Distribution Center)

The industrial sector has enjoyed exceptional growth over the past few years, driven in part by the continued strength of e-commerce as a share of total retail sales and the impact of manufacturing reshoring and nearshoring initiatives. Construction has ramped up quickly since the beginning of the COVID-19 pandemic in response to intense demand. The annual rate peaked at 283 million square feet by mid-2023. As the market grew more balanced, construction started to slow amid higher interest rates and cooling demand. Completions declined steadily from 85 million sq ft at the end of last year to only 24.3 million sq ft in Q4, down more than half from just a quarter ago.

Demand for warehouse and distribution center space cooled as consumption shifted from goods to services, and high interest rates challenged inventory management. Net absorption in the fourth quarter was down 65% from the quarter ago to 8.8 million sq ft, only a fraction of its peak volume in Q3 2021. It is worth noting that net absorption teased negative territory at -438,000 sq ft in December, the first time since 2009! As demand cooled more rapidly than supply, the vacancy rate extended its upward trajectory established in mid-last year and climbed another 20 basis points to 5.4% at the national level in this quarter. Although vacancy increases reflected market rebalancing, the level remained significantly lower than the sector’s pre-pandemic average. As a result, the growth of asking and effective rent slowed but stayed positive at 0.8% and 0.5%, respectively, in Q4.

Figure 4: Industrial (Warehouse/Distribution Center) Rent and Vacancy Trends Vacancy Trends Continue an Upward Climb After Years of Historic Construction While Remaining Below Pre-Pandemic Levels

Moody's Analytics CRE

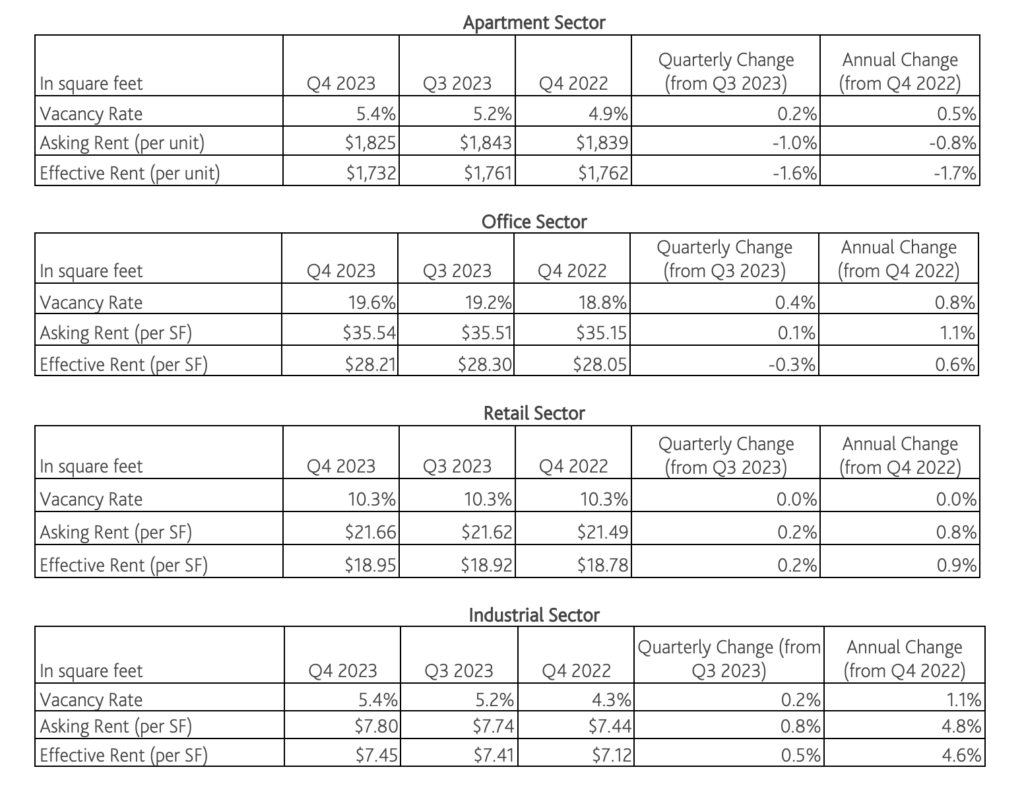

Table 1: Summary of Moody’s Analytics CRE Q4 2023 Statistics

Moody's Analytics CRE

US Metros

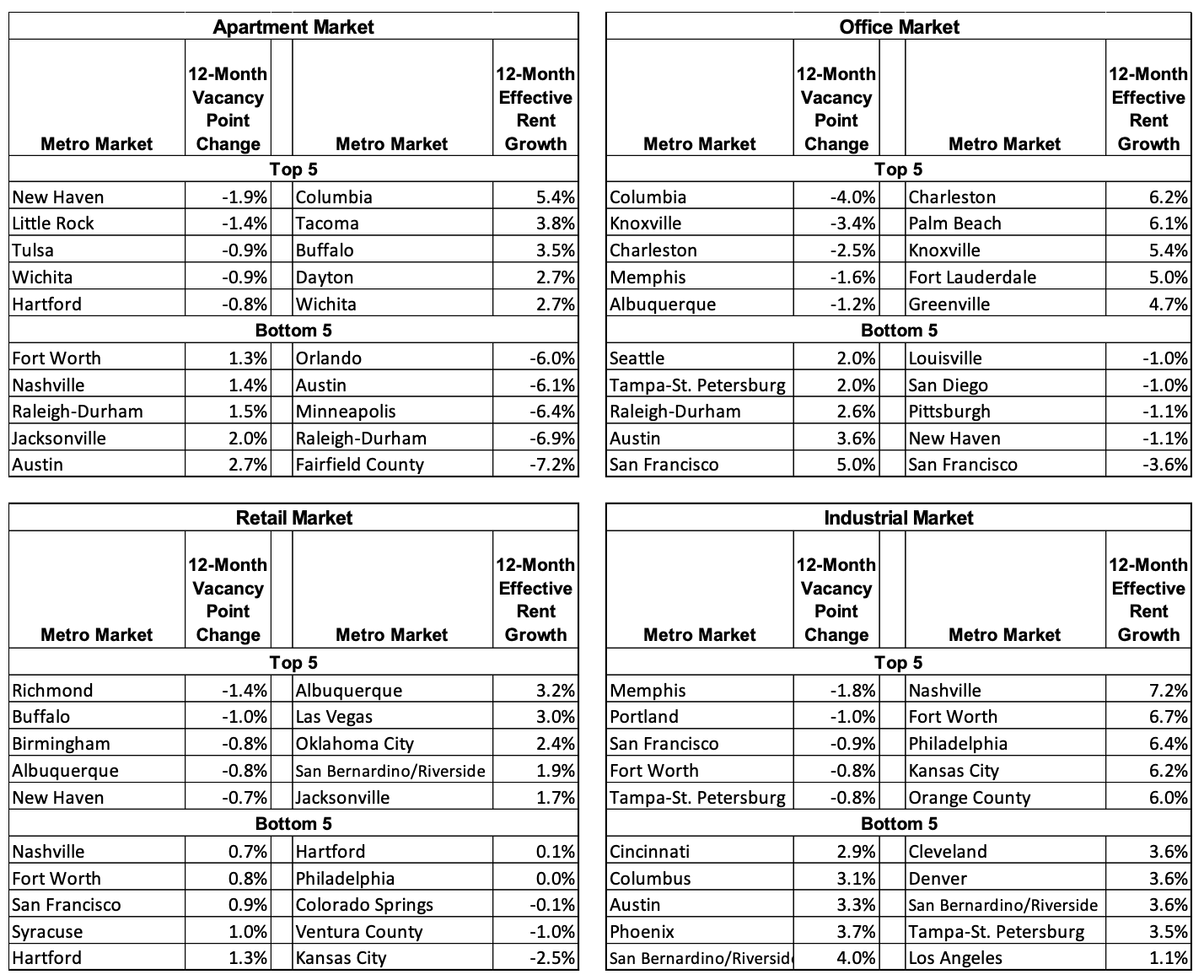

For multifamily, 1 in every 5 metros recorded over 2% of inventory growth in 2023, while nearly 60% (47 of 79) of primary metros had more move-outs than move-ins in the last quarter of the year. Nashville (5.2%), Jacksonville (4.1%), Austin (4.0%), Phoenix (4.0%), Charlotte (3.7%), Salt Lake City (3.7%), and Fort Lauderdale (3.0%) were leading the annual inventory growth among all. With little surprise, all of them suffered from year-over-year vacancy increases, ranging from 0.6% in Charlotte and Fort Lauderdale to 2.7% in Austin. Except for Salt Lake City, which was supported by more balanced market demand, all of the aforementioned metros also recorded notable annual effective rent declines, ranging from -1.3% in Nashville to -6.1% in Austin. In the final three months of the year, over 90% of all primary metros have experienced quarter-over-quarter vacancy increases, more than half of which also recorded rent declines at the same time. Nineteen primary metros recorded over 2% of asking rent declines in the fourth quarter, with Orlando (-3.8%), New Haven (-3.2%), Omaha (-3.2%), and Fort Worth (-3.1%) topping the list.

For offices, San Francisco (-4.4M sqft), Los Angeles (-2.4M sqft), Philadelphia (-2.0M sqft), Washington, DC (-1.4M sqft), Seattle (-1.3M sqft), Denver (-1.2M sqft), Orange County (-1.2M sqft), Baltimore (-1.1M sqft), and Raleigh-Durham (-1M sqft) each recorded more than 1 million sqft of negative net absorption in 2023. In the fourth quarter alone, Moody’s Analytics preliminary data showed over half (50 of 79) of US primary metros experienced negative absorption. San Francisco led the loss in Q4 with -2,400,000 sqft of net move-outs, while Washington, DC, and Chicago had over 100,000 sqft. Fifty-two primary office markets experienced vacancy increases in 2023, among which San Francisco (+5.0%), Austin (+3.6%), and Raleigh-Durham (+2.6%) significantly underperformed. Effective rents fell the most over the past 12 months in San Francisco (-3.6%), New Haven (-1.1%), Pittsburgh (-1.1%), San Diego (-1.0%), and Louisville (-1.0%), each experiencing a greater than -1.0% decline.

Retail vacancies declined or remained flat across 47 primary metros in Q4, but the changes were mostly moderate and stable, indicating the national trend was widespread. Retail vacancy changes ranged from -60 bps in New Haven to +100 bps in Syracuse, but only 6 of our 77 primary metros observed a shift of 40 bps or greater. Over 2023, retail star performers included Richmond (-140 bps), Buffalo (-100 bps), Birmingham (-80 bps), and Albuquerque (-80 bps), while Hartford (+130 bps), Syracuse (+100 bps), and San Francisco (+90 bps) experienced the sharpest rises in retail vacancy. Seventy-three of 77 primary markets recorded effective rent growth compared to a year ago, but Kansas City (-2.5%), Ventura County (-1.0%), and Colorado Springs (-0.1%) experienced declines while Philadelphia (0.0%) held flat.

Finally, over half of the primary industrial markets recorded negative net absorption in the final quarter of 2023. On a year-over-year basis, nearly 3 out of every 4 primary metros experienced higher vacancy. Five metros recorded more than 5% of warehouse-distribution space growth for the year, which are Austin (12.5%), Phoenix (10.5%), San Bernadino/Riverside (6.2%), Jacksonville (6.2%), and Fort Worth (5.1%). Aside from Fort Worth, which was supported by its unique advantages of an expandable market, affordable rent, and central location for logistics, other rapidly growing industrial markets all recorded year-over-year vacancy growth ranging from 1.9% in Jacksonville to 4.0% in San Bernadino/Riverside. Los Angeles lagged behind other industrial markets due to more than 6 million square feet of move-outs throughout the year.

*These retail statistics represent neighborhood and community shopping centers only. Moody’s Analytics CRE does not report mall rents at the metro level.

Table 2: Annual Effective Rent Growth and Vacancy Changes: Top 5 and Bottom 5 Metros

Moody's Analytics CRE

The US economy is gradually coming out of the good-news-is-bad-news paradox. Consumer confidence surged in the final month of 2023, which set the premise for another good year ahead. As inflation heads further in the right direction, rate cuts may finally be on the horizon. That will be welcome news for CRE transactions and the overall business environment. In the meantime, space market rebalancing and credit risks associated with CRE lending must be cautiously calibrated, monitored, and prepared for.

Each CRE sector has its own challenges and opportunities. The office's painful evolution depends on how the “Great Compromise” will set the broader return-to-office (RTO) policy in the near term. A glimmer of hope was ignited by a reset of property values (and therefore rent), especially in metros with the highest price per square foot. The multifamily market expects more projects to come online in 2024, as many projects in the pipeline faced delays due to capital constraints in the year prior. In contrast to the glut of supply will be the normalization of demand, driven by slowed population growth and (hopefully) renters moving up the homeownership ladder. Affordability continued to pressure renter households, especially those at the lower end of the income distribution. Retail was mostly in a holding pattern in recent quarters; lower-income households had to limit goods and service consumption due to elevated costs of living, the resumption of student loan payments, and the higher principal and interest on other debt. But lower interest rates may finally help retailers reconsider expansion, franchising, or even mergers and acquisitions. Regardless of a reliance on commuting workers, experiential retail and mixed-use communities are ever more appealing to local residents, businesses, and consumers. The industrial sector may have passed its golden period of growth due to the unexpected destruction of the supply chain over the past few years, but the revolution in inventory management and the requirement of warehouse/flex space for the important e-commerce industry continue to recalibrate the market equilibrium.

Space market challenges will pose potential risks to associated commercial loans, especially if the underlying collateral faces greater uncertainty with its performance metrics. That is indeed concerning for mid-size to smaller financial institutes, which have significant CRE exposures. But so far, Moody’s Analytics CRE does not believe this will become a source of systematic risk for the overall banking system. In 2024, we expect to see greater integration of live, work, and play communities to drive the formation of the space market’s new norm. Among many challenges, there will be abundant opportunities for market participants to invest in this new era if they believe in the future of commercial real estate.

Investors are flocking to student housing as its rent growth outpaces traditional multifamily properties, lured by its resilience during economic downturns and higher-than-average returns.

Billions Funneled into Student Housing as Rent Growth Exceeds Apartment Market

Investors are flocking to student housing as its rent growth outpaces traditional multifamily properties, lured by its resilience during economic downturns and higher-than-average returns.

Rising star: Major investors are pouring billions into the student housing market attracted by its higher rent growth, outperforming traditional apartments. The off-campus student housing sector saw a 7.1% rent increase over six months, with some universities noting growth above 20%. Seen as "recession-proof," investments are especially concentrated in Sun Belt states, known for their substantial rent and enrollment hikes. However, this trend has raised concerns over the capacity of campus housing.

Student housing rent growth this year has far outpaced previous years, data from Yardi Matrix shows.

Student housing vs. apartment market: While student housing rents have surged, apartment rents have begun to plateau after reaching record highs in the past. For instance, student housing rent growth this year has substantially surpassed previous years, with data indicating a marked increase in rent growth rates. In contrast, multifamily property rents rose at a more modest rate, making student housing a more appealing investment.

Major deals: BREIT's acquisition of American Campus Communities for $13B last year underscored the growing appeal of student housing in the commercial real estate market. In addition, Blackstone's ACC has initiated two major student housing projects within its $3B program. However, as student enrollments rise, many universities struggle to provide adequate housing, leading to local market imbalances. Cities such as Boston, for instance, are experiencing shortages in off-campus apartments.

Shifting tides: Investor interest in student housing is now leaning towards luxury properties near campuses. Last year saw record property sales in this sector, with over $10B invested for two straight years. However, 1H23 saw a slower investment pace due to higher rates, changing the investor landscape. Investment funds made up 52% of deals in 1H23, a jump from 12% in 2H22, while universities and public REITs reduced their participation. There's also a spike in foreign investment, especially from the Middle East and Asia.

➥ THE TAKEAWAY

Campus housing crunch: The booming student housing sector is a double-edged sword. On the one hand, it's attracting significant investment, but on the other, it's amplifying accommodation issues in university towns. With universities experiencing record enrollments, there's an urgent need to house the growing student body without overburdening local housing markets. As enrollments surge, investors are faced with the challenge of benefiting from this growth while also addressing the housing deficits in academic communities.

For renters who've felt the sting of rapidly increasing costs, there's a sigh of relief on the horizon. The rapid inflation of rent prices, which has been a pressing concern for many in recent years, is showing signs of stabilization.

From Skyrocketing to Stabilizing: The New Era of Rental Prices

Analysis based on average monthly rent data for provided by CoStar Group. The data includes newly posted rents, not lease renewals, for 1,660 counties for June of each year from 2019 to 2023. Counties with fewer than 1,000 multi-units, according to Census Bureau data, were excluded.

Good news is on the horizon for renters: The rapid escalation in rental prices, which had previously seemed unstoppable, appears to be taking a pause.

Rental rollercoaster: Between 2020 and 2022, rents surged by a striking 15%, the most rapid increase in nearly a century. However, the fervor has calmed. Rent growth has reverted to pre-pandemic rates, seeing an annual growth of about 1 to 3 percent. Interestingly, in cities that recently witnessed surging rents like Austin and Atlanta, prices are now dropping. As Igor Popov, chief economist at Apartment List, observes, the rental market is "taking a breath.

Why the slowdown? A significant factor in this slowdown is the surge in housing construction. An impressive nearly 1 million new apartment units are currently under construction nationwide. By the end of 2023, over half of these are expected to be on the market. Concurrently, the demand for rentals is waning as the U.S. adjusts to post-pandemic life. The appetite for apartment living has decreased, with fewer individuals moving out and more staying in familial homes. This change has created a discrepancy between available apartments and interested renters, thereby stabilizing price growth.

The Sun Belt phenomenon: The Sun Belt region, which includes parts of the Southern U.S., experienced a unique scenario. Initially, during the pandemic, there was a spike in demand as individuals sought warmer climates and more affordable living conditions, moving away from urban centers like New York. This shift led to a boom in rental prices in cities like Phoenix, Dallas, and Miami. However, the rush to meet this demand has led to an oversupply, causing rents to stabilize and even decrease in some areas.

➥ THE TAKEAWAY

The new normal: While renters can find solace in stabilizing prices and even some reductions, it's crucial to note that the cost of renting remains substantially higher than pre-pandemic levels in many areas. Areas like Atlanta, despite witnessing recent rent reductions, still have renters paying substantially more than before the pandemic. The introduction of incentives like months of free rent indicates a market adjusting to new realities, but the days of pre-pandemic affordability seem to be a distant memory for now.

Plus: CoStar's analysis shows a continued dip in CRE sale prices in October, aligning with the ongoing trend of increased rates.

Leasing Surge in Mid-Priced Apartments with Improved Economy

In 2023, the U.S. multifamily market has seen a significant upswing in renter demand, especially for mid-priced apartments rated three stars. This shift marks a recovery from a sluggish performance in the latter half of 2022.

A surge in demand: There has been a 77% increase in occupancy over the last year, with 260,000 more units being filled than vacated. This surge is primarily in mid-priced, three-star properties, contrasting with the disappointing absorption of only 146,000 units in 2022.

Influencing the market: The market slump in 2022 was driven by a combination of high inflation, increased oil prices, and recession fears, which significantly impacted consumer confidence and demand, especially in mid- and low-priced properties. This led to renters seeking more affordable housing solutions or delaying household formation.

Improving economy: The rebound in 2023 has been fueled by improved consumer confidence, lower inflation, strong wage growth, and reduced recession fears. These factors have notably increased the demand for three-star properties by 54,000 units in the first three quarters of the year.

➥ THE TAKEAWAY

Positive outlook: The high-end segment of the market, comprising four- and five-star properties, has remained stable, thanks to the lower rent-to-income ratio of its renter households. Looking ahead, if the economy avoids a recession, multifamily demand could return to pre-pandemic levels by 2024, although supply is expected to exceed demand for the third consecutive year.