Comparing a Deferred Sales Trust vs Delaware Statutory Trust is one of the most critical steps for multifamily owners who want to sell but are paralyzed by the looming threat of capital gains taxes.

As a multifamily investment sales broker, I frequently speak with owners who are exhausted by property management. They want to sell, but they refuse to hand 30% to 40% of their equity over to the IRS, and they certainly do not want to buy another apartment building to manage.

In our recent guide on crafting a successful Chicago multifamily disposition strategy, we highlighted absolute triple-net (NNN) leases and the Delaware Statutory Trust (DST) as powerful 1031 exchange vehicles to solve this exact problem.

However, as you research these exit options, you will almost certainly run into a confusing roadblock: there is another DST out there.

Promoters heavily market the Deferred Sales Trust as a 1031 alternative, promising high yields and stock market flexibility. Because they share the exact same acronym, sellers often mistake them for the same thing. They are not.

When conducting a true comparison of a Deferred Sales Trust vs Delaware Statutory Trust, you must understand that they rely on completely different tax codes, hold entirely different assets, and carry drastically different risks. By understanding these options, you can confidently list and sell your property knowing your wealth is protected.

Here are four key facts to tell the two DSTs apart.

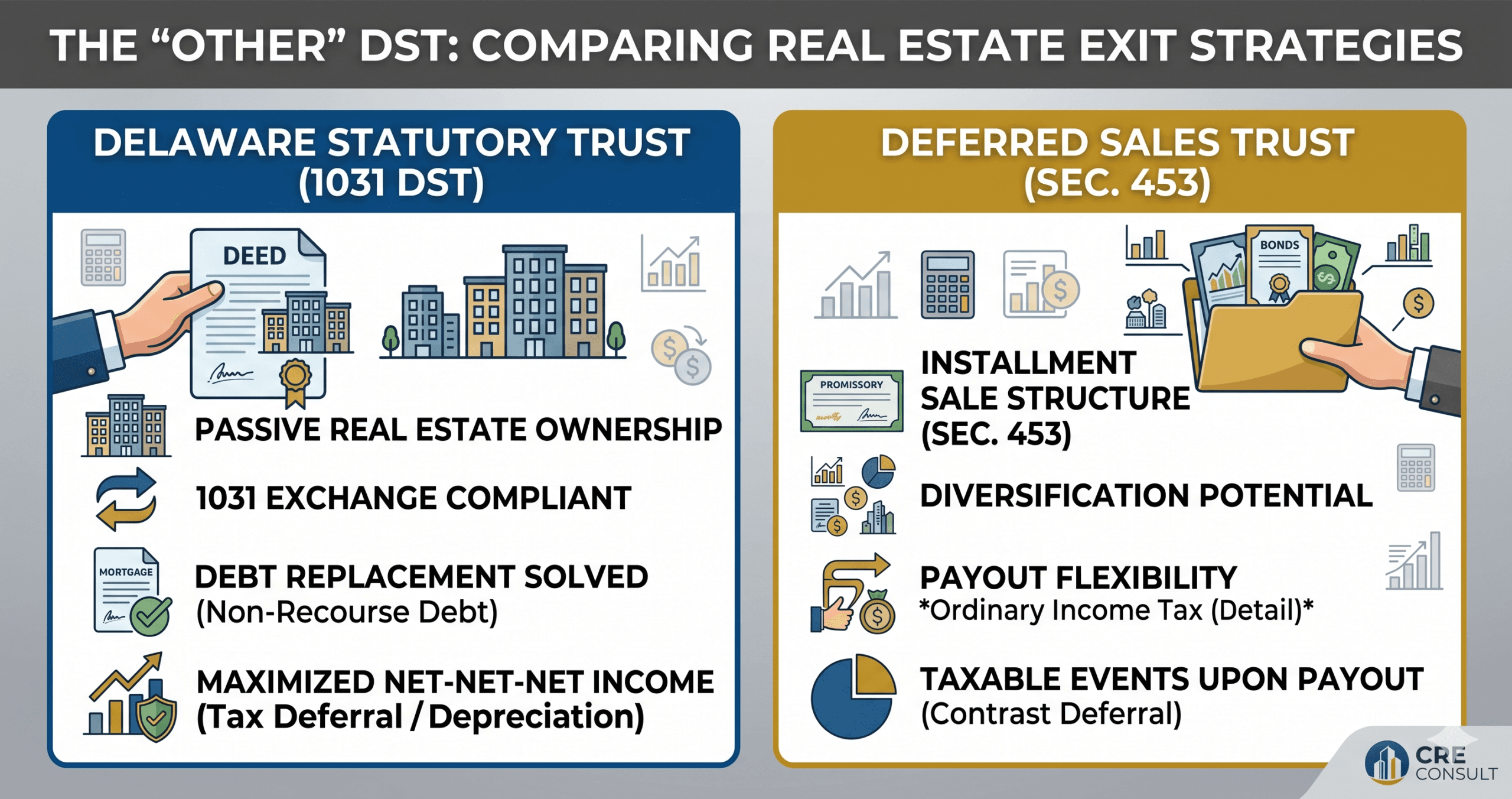

1. The Legal Framework: Section 1031 vs. Section 453

The foundational difference in a Deferred Sales Trust vs Delaware Statutory Trust setup lies in how they interact with the IRS tax code.

The Delaware Statutory Trust (The Real Estate Route) This structure operates under the standard 1031 exchange. When we sell your multifamily property, you reinvest your proceeds into a fractional share of institutional-grade, physical real estate. This could be a massive data center, a medical facility, or a 300-unit apartment complex. You remain invested in tangible real estate and preserve your wealth without the headaches of day-to-day management.

The Deferred Sales Trust (The Stock Market Route) This structure relies on the installment sale rules found in IRC Section 453 (External Link). Instead of buying new real estate, you sell your property to a specialized trust in exchange for a promissory note. The trust then sells the property to the final buyer for cash and invests that cash into traditional financial markets (stocks, bonds, and mutual funds) to fund your monthly note payments.

2. The Yield Illusion: Gross Payout vs. Net After-Tax Income

In the battle of yield between a Deferred Sales Trust vs Delaware Statutory Trust, many commercial investors are drawn to the installment option because promoters might promise a 6% to 8% payout. This looks attractive compared to the 4.5% to 5.5% cash-on-cash returns typical of today's real estate funds.

However, savvy sellers know you must look at the net-net-net after-tax return.

- The Ordinary Income Trap: Every dollar paid out from a Deferred Sales Trust promissory note is taxed as ordinary income. If you sit in a higher federal tax bracket, up to 40% of your Deferred Sales Trust income will be instantly eaten by taxes. A 7.5% gross yield quickly shrinks to a 4.5% net yield.

- The Real Estate Tax Shield: By contrast, the income from a Delaware Statutory Trust is heavily sheltered by real estate depreciation. Because you own physical property, you receive a "phantom" expense deduction. Often, 50% to 70% of your DST yield is completely shielded from current-year income taxes.

The reality is that the actual take-home cash in your pocket is often nearly identical between the two, but the Deferred Sales Trust requires you to take on stock market volatility to get it.

3. The Fully Depreciated Property and the "Debt Trap"

If you have owned your apartment building for decades, you have likely fully depreciated the asset, meaning your cost basis is zero. This scenario exposes a massive hidden risk. A major deciding factor between a Deferred Sales Trust vs Delaware Statutory Trust is how they handle your existing mortgage.

To completely defer your taxes in a real estate transaction, the IRS requires you to replace whatever debt you pay off at closing.

- Delaware Statutory Trust Advantage: These funds come with pre-packaged, non-recourse debt baked right into the structure. If you need to replace $1 million in debt, you simply buy into a leveraged fund, effortlessly satisfying the IRS requirement without ever signing a personal loan document.

- Deferred Sales Trust Risk: A Deferred Sales Trust does not replace debt. The mortgage is simply paid off at closing. However, if your mortgage balance is higher than your depreciated cost basis, the IRS treats the difference as a "constructive payment." This triggers a massive, immediate tax penalty. A Deferred Sales Trust cannot protect you from this "debt over basis" trap.

4. Estate Planning: Generational Wealth Transfer

How do these structures perform when it is time to pass wealth down to your family? For legacy planning, a Deferred Sales Trust vs Delaware Statutory Trust offers vastly different outcomes.

If you hold a Delaware Statutory Trust until you pass away, your heirs inherit the physical real estate with a "step-up in basis." This incredible IRS provision effectively wipes out decades of deferred capital gains and depreciation recapture taxes, allowing your family to inherit the full value of the asset tax-free.

If you pass away while holding a Deferred Sales Trust, your heirs simply inherit the remaining balance of the promissory note. This is treated as "Income in Respect of a Decedent" (IRD). There is no step-up in basis, meaning your heirs inherit your tax liability along with the note.

Evaluating a Deferred Sales Trust vs Delaware Statutory Trust to Facilitate Your Sale

At the end of the day, my job as a multifamily investment sales broker is not to sell you trust products. My job is to help you successfully sell your property at the absolute highest market value and guide you toward the right exit strategy so you can actually keep your profits.

Ultimately, choosing between a Deferred Sales Trust vs Delaware Statutory Trust comes down to your ultimate financial goals and risk tolerance. If capital gains tax concerns are the only thing keeping you from listing your property and moving on to your next chapter, you have powerful options available to you.

By bringing in the right 1031 accommodators and financial planners, we can structure a highly profitable sale that transitions you out of the landlord business and into stable, passive retirement income.

Are taxes holding you back from selling? Let's discuss your options. Contact Randolph Taylor and the team at CRE Consult today to explore a disposition strategy tailored to your property.

https://creconsult.net/deferred-sales-trust-vs-delaware-statutory-trust/?fsp_sid=2508