9301 West Golf Rd | Des Plaines, IL 60016

Broker: Randolph Taylor rtaylor@creconsult.net | 630.474.6441

https://www.creconsult.net/golf-sumac-professional-building-medical-office-space-for-lease-9301-golf-rd-des-plaines-il-60016/

Commercial property sales generated over $400 billion in transaction volume in 2020, with apartment buildings for sale and office properties leading the charge. However, one of the biggest challenges that commercial building owners face is understanding when and how to sell.

This article explores some of the primary exit strategies commercial property sellers use to market a commercial building.

Sophisticated commercial real estate investors always have an exit strategy to help maximize profits by selling when the time is right. There are three main exit strategies to consider when selling commercial real estate:

Commercial real estate loans have a 25-year amortization with a 5- or 10-year term. Even though monthly loan payments are amortized over 25 years, the loan will be called or due between five and ten years. Rather than refinancing the existing loan, some investors begin the building sale process at least 12 months before the loan is expected to mature.

The net operating income (NOI) a property generates largely determines the commercial real estate value in space for rent. In a 6% cap rate market, a building with an annual NOI of $500,000 is worth about $8.3 million ($500,000 NOI / 6% cap rate). On the other hand, a property with an NOI of $300,000 in the same market is valued at $5 million. Once a commercial building is leased up and reaches maximum occupancy, it may be the perfect time to sell.

Many commercial real estate investors hold the property and collect cash flow until significant capital expenditures (CapEx) are on the horizon. Items such as replacing a roof or repaving a parking lot can take a serious bite out of profits. Owners who aren’t willing to invest additional capital in their property may decide to sell to another investor, even if the selling price is slightly below market.

When the time is right, there are three main ways for an investor to sell commercial real estate, including lots of land or apartment complexes for sale:

1. Sell directly to another investor: Motivated buyers with financing arranged or cash in hand may be willing to close quickly on the right property at the right price. Sellers should know the fair market value of their property by ordering a commercial appraisal and compiling buyer documents to help the buyer move fast.

2. Work with a commercial real estate broker: Depending on the market size, commercial brokers may specialize in specific real estates niches, such as medical office space or workforce multifamily housing. A good broker will guide an investor through the selling process from start to finish, although sellers should plan on paying a sales commission of between 4% – 10% depending on property type and sales price.

3. Sell as an FSBO: “For sale by owner” commercial real estate deals are prevalent in some markets. FSBO sellers choose to represent themselves and cooperate with buyers represented by a commercial real estate broker. Because there’s no co-broker involved, sales commissions are usually less. However, sellers representing themselves must understand the local retail real estate market trends to avoid leaving money on the table by selling too low.

Before listing a commercial building for sale, sellers should gather the documents buyers need. Having the correct information makes it easier to attract qualified buyers and avoids having the property fall out of escrow due to unknown defects:

Sellers should do these things before listing and marketing a commercial building:

Hire a professional inspector to review the overall condition of the building and identify necessary repairs. This prevents a seller from being caught off guard when a buyer does its inspection once the property goes under contract.

Make the repairs discoverable by the pre-listing inspection to help increase the sales price. Sellers who sell with deferred maintenance can adjust the asking price accordingly, letting a buyer know the lower price is compensation for repairs that need to be made.

After repairs have been made, hire a certified commercial real estate appraiser to walk through the property, run comparables, and determine fair market value. Factors affecting commercial property appraisal include location, rent roll, property condition, market trends, and recent sales of comparable properties in the market or submarket.

Sellers should be prepared to proactively find the most qualified buyers for their property instead of waiting for a buyer to come. Essential parts of a commercial real estate marketing campaign include:

Understanding the transaction from both sides of the closing table helps savvy owners sell fast and for a fair price. By knowing the local commercial real estate market and comparing similar properties, sellers can better appreciate and communicate the actual value of their commercial building to potential buyers.

Source: The Basics of a Commercial Building Sale | Crexi Insights

https://www.creconsult.net/market-trends/the-basics-of-a-commercial-building-sale/

For decades, real estate investors have applied tax deferral strategies like the 1031 Exchange to avoid paying capital gains taxes on high-value assets. SDIRAs, qualified opportunity funds, tax-loss harvesting, primary residence exclusions, and 1031 exchanges can all defer capital gains taxes on the property. However, these deferral strategies often rely on the type of property and the tax filing status of their owners. Real estate investors commonly use IRS Code Section 103 to exchange properties, thus transferring and deferring tax payments.

Pending changes to the IRS tax code could impede attempts to defer capital gains taxes through Section 103. The Biden Administration desires to curtail like-kind exchanges of high-value properties in coming years. The changes could affect the tax burden on various investment property owners. It could impact those who rent out vacation cabins and those who manage multi-unit properties. Follow below to learn more about 1031 exchanges and how proposed legislation could affect the ability of investors to defer real estate taxes by tightening 1031 exchange rules.

According to a recent article by Grace Enda and William G. Gale for The Brookings Institute, "a capital gain is the increase in value of an asset over time." Technically, write Gale and Enda, "a capital gain is a difference between an asset's current value and its' basis,'" with the basis representing a property's "cost to the owner." When the value of an asset increases over time, investors must, by tax law, repay some of that accrued value in the form of capital gains tax. This property tax bill becomes due at the time of sale.

Theoretically, property owners can use proceeds from the sale to pay off any capital gains in property taxes based on the accrual of value throughout ownership. Capital gains taxes apply only to realized profits, not unrealized profits based on assessed value, which is how capital gains taxes differ from annual property taxes. As such, capital gains property taxes are not levied on property currently within an owner's possession.

There are two types of capital gains taxes imposed by the IRS: short-term and long-term capital gains. In his article "Capital Gains Tax" for Investopedia, Jason Fernando explains that long-term capital gains apply to assets listed for sale after at least one year of ownership. According to Fernando, property sold after at least a year of ownership is subject to capital gains taxes at rates of "0%, 15%, or 20%, depending on the taxpayer's tax bracket for that year."

Short-term capital gains tax applies only to property the owner holds for under a year. In these cases, profit from a property's sale is "taxed as ordinary income." Properties for under a year are usually subject to much higher tax rates than the long-term capital gains tax. Real estate investors often seek ways to defer because capital gains tax can be as much as 20% of a property's sale price.

There are a few legal methods by which real estate investors can defer capital gains taxes. In his article "How Do I Avoid Capital Gains Tax When Selling a House? ", Certified Financial Planner Matt Frankel outlines five standard methods. According to CFP Frankel, property owners can defer capital gains tax post-sale through SDIRAs, qualified opportunity funds, tax-loss harvesting, primary residence exclusion, and 1031 exchanges.

SDIRAs allow future property owners to defer this tax by "owning real estate within a retirement account" (Frankel). Property owned within a self-directed IRA is not subject to capital gains taxes upon sale, even when "you sell for a profit." Taxes are only due when you finally withdraw from your IRA.

Qualified opportunity funds are another way property owners defer capital gains tax. Opportunity funds encourage real estate investors — usually developers — to invest in economically depressed areas, often designated opportunity zones. A state or local government might offer tax incentives to encourage developers to invest in underserved communities. These tax incentives might include reduced, deferred, or forgiven taxes on capital gains.

Another way real estate investors avoid taxes on capital gains is through tax-loss harvesting. For Forbes, John Schmidt and Rebecca Baldridge explain tax-loss harvesting as "when you sell some investments at a loss to offset gains you've realized by selling other stocks at a profit" (Can Tax Loss Harvesting Improve Your Investing Returns?)."

What does this mean? You only pay taxes on your net profit or the amount you've gained minus the amount you lost, which can reduce your tax bill significantly. In addition to lowering taxes owed, real estate investors often engage in tax-loss harvesting because it "frees up cash so you can buy new assets that may be more likely to generate positive performance."

Identifying a property as one's primary residence can lower one's tax burden. In her article "What Is the Section 121 Exclusion?", Lea Uradu explains that Internal Revenue Service Section 121 "allows homeowners to exclude up to $250,000 ($500,000 for joint filers) of capital gain from the sale of their primary residence."

With a primary residence, only capital gains exceeding this amount are reported and subject to CG taxes. While Section 121 is helpful for homeowners and often a life-saver, it rarely helps real estate investors with multiple properties. There are a few exceptions, however. If a property owner chooses to live in their rental property several years before selling, they could limit the CG taxes that come due when the property sells.

In his article "How Do I Avoid Capital Gains Tax When Selling a House? "Matt Frankel identifies 1031 exchanges as "the most effective, commonly used strategy by real estate investors to avoid capital gains taxes." For those unfamiliar with the term, 1031 exchanges are also called "like-kind exchanges." One thousand thirty-one exchanges allow the owner of an investment property, such as a rental property, to sell their property and "use the proceeds to buy another investment property."

Until this new property is acquired, taxes on capital gains are deferred. When one wishes to sell this newly purchased property, the owner can "complete another 1031 exchange." This allowance permits property owners to "use the 1031 exchange strategy to defer capital gains tax indefinitely."

Writing for Investopedia in his article "1031 Exchange Rules: What You Need to Know," Robert W. Wood explains like-kind exchanges in further depth. Wood notes that though 1031 exchanges allow real estate investors to defer taxes on capital gains, several restrictions exist. For instance, 1031 exchanges apply only to qualifying like-kind sales of property or other assets. Typically, a replacement property is of equal or more excellent value than the original asset. Misunderstanding the properties and situations to which 1031 exchanges apply could legally and financially imperil investors.

While the rules surrounding like-kind exchanges are "surprisingly liberal," Wood writes that "there are traps for the unwary." Special 1031 exchange rules apply to rental properties, vacation homes, and depreciable properties.

Recent changes to the Internal Revenue Code have tightened restrictions on applying 1031 exchanges to rental properties, particularly vacation homes. In 2018, the Trump administration altered the legal definition of 1031 exchanges. From then on, 1031 exchanges applied only to real estate. Additional charges are expected in the coming months under the Biden Administration.

In his article "1031 Exchange Rules: What You Need to Know" for Investopedia, Robert W. Wood notes that like-kind exchange rules apply to timing, property type, and property value. First, Wood identifies two current 1031 exchange "timing rules." These include the forty-five-day Rule and the one-hundred-eighty Rule. According to Wood, the first timing rule relates to classifying one's replacement property. After a property sells, proceeds from the sale transfer to a qualified intermediary. The property seller cannot take possession of these proceeds until the initial forty-five-day period has expired. Otherwise, one could "spoil the 1031 treatment."

The seller must also inform the qualified intermediary that they intend to designate a replacement property during this period. The replacement property must be specified to the qualified intermediary during this time. If you are unsure which property to acquire, you can identify up to three properties to your qualified intermediary.

Of course, there is a second timing-related delayed exchange rule. The 180-Day Rule requires a seller to complete the purchase process of their replacement property within one hundred eighty days after selling their relinquished property. There may be a gap between the first property's sale price and the replacement property's purchase price. If this occurs, the real estate investor must pay CG taxes on this amount. Sometimes, this profit from real estate investing can be offset and exempted from immediate taxation. Investors must remember that 1031 exchange rules vary from state to state.

One thousand thirty-one exchanges require investors to exchange a relinquished property for a like-kind replacement property. As such, property owners cannot replace the personal property with investment property and vice versa, expecting to defer tax on capital gains. Matt Frankel explains in his article "1031 Exchanges: The Basics, Rules, & Requirements ". The Certified Financial Planner explains that in a 1031 exchange, "you can't sell an investment property, acquire a vacation home for you and your family, and call it a 1031 exchange." However, property owners can "sell a single-family rental home and acquire a retail building, as long as both assets" are business or investment properties.

There are ways to defer payment of capital gains during a vacation home or rental property sale. Robyn A. Friedman explains in the article "A Treasured Tax Break for the Smart Real-Estate Investor" for The Wall Street Journal. According to Friedman, property owners can convert their vacation home "from personal use to business use by renting it out for at least 14 days a year for two successive years before the sale." After this two-year period has concluded, the owner can exchange their vacation home and "defer capital-gains taxes as long as they continue to rent for a minimum of 14 days a year for two years after the sale." However, property owners must remember that only real property is covered. Friedman writes that "personal property is excluded from like-kind exchanges." Property owners should also not forget that rules surrounding tax-deferred in 1031 exchanges will likely change during the Biden Administration.

Rules surrounding deferred exchange and real estate tax as defined by the Internal Revenue Code could change significantly in the coming months as the Biden Administration weighs their consequences and benefits. According to Will Parker in his article "Biden Proposal Would Close Longtime Real-Estate Tax Loophole" for The Wall Street Journal, Biden's proposal would "abolish 1031 exchanges on real-estate profits of more than $500,000" for a single person. Any amount over $500K (or $1 million for married couples) could not be deferred and would be subject to annual tax on capital gains.

Parker writes that the desire to abolish exchanges of high-value properties has arisen from a flaw in the tax code design. According to Parker, "in theory, capital-gains tax from these deals eventually gets paid." However, many of today's real estate investors "buy and sell properties this way until they die, passing the capital gains on to their heirs tax-free at death."

Sometimes, investors pass capital gains taxes from commercial real estate, like multi-unit property for sale. The Biden Administration believes that these loopholes in Section 103 "disproportionately allow the very wealthy to avoid taxation." In addition to eliminating 1031 exchanges on high-value properties, the new administration plans to change the capital gains tax rate. This administration hopes to "raise the top rate paid on capital gains and dividends to 39.6% from 20%."

As Lynn Mucenski Keck writes in her article "Like-Kind Exchanges To Be Limited Under Biden's Tax Proposals," changes to the Internal Revenue Code are challenging to implement. According to Keck, "many practitioners are still grappling with the impact of the TCJA on their tax planning." For those unfamiliar, the TCJA refers to the Tax Cuts and Jobs Act of 2017. Keck writes that the Biden Administration plans to implement their new changes to Section 103 by the end of 2021.

As such, the new "limited 1031 deferral provision [would apply to] exchanges completed in tax years after December 31, 2021." Those who have entered into exchanges under today's tax code would still be able to take full advantage of the 180-day time slot currently allotted. Though adjusting to these changes to Section 103 might be difficult, this buffer should help real estate investors and their financial planners navigate new property exchange rules.

Source: Everything to Know About a 1031 Exchange | Crexi Insights

https://www.creconsult.net/market-trends/everything-to-know-about-a-1031-exchange/

In most commercial real estate transactions, the buyer finds a property, negotiates a purchase contract with the seller, obtains financing from a commercial lender, and closes escrow.

However, a growing number of property owners are discovering that they can directly provide financing to buyers to sell property faster, ultimately generating more potential profits from interest income.

Owner financing for commercial properties gives buyers and sellers more control over the transaction and enormous profits by cutting out the traditional commercial lender as a middleman.

Some commercial properties for sale by owner (FSBO) offer buyers owner financing. When a real estate sale by the owner occurs, the seller accepts regular monthly payments directly from the buyer instead of the buyer having to go through the time, trouble, and expense of obtaining a commercial real estate mortgage.

Depending on the market in which the investment property for sale by the owner is located, owner financing may go by a different name.

The terms seller financing, owner carryback, the owner will carry, carrying the note, commercial owner financing, and the owner brought financing are all used to describe owner financing. In some regions, owner financing is referred to as a ‘land contract,’ even if the property is a building versus commercial land for sale by an owner.

There are several benefits and potential drawbacks to buyers and sellers who agree to owner financing:

Now let’s look at an example of how owner financing in commercial real estate can work.

In this scenario, we’ll assume the owner is offering owner financing to sell a difficult property, reduce upfront capital gains tax liability, and earn interest income. The buyer benefits by making a lower down payment and getting a very fair price on the property at an attractive interest rate:

The terminology used and structure of an owner-financing mortgage document (also known as a promissory note) is similar to what traditional commercial real estate lenders use:

Amortization is the schedule of periodic payments, including principal and interest. In the above example, the owner carryback amount of $1,800,000 is amortized over 30 years even though the loan term is for ten years.

The loan term is until the borrower must pay off the remaining balance. While most residential mortgages have 30 years, commercial real estate loans typically have terms of 5, 10, or 15 years. In our example, the time of the owner-financed loan is ten years.

The balloon is the remaining loan balance principal that must be paid at the end of the loan term. In the above example, the seller receives a $1,542,928 balloon payment in addition to the periodic mortgage payments already received from the buyer. The buyer and seller could agree to finance the remaining principal balance with a new owner financing note, or the buyer could obtain financing from a traditional commercial lender.

A promissory note details the terms and conditions of the owner-financed mortgage, including:

Owner financing for commercial property can create a win-win situation for sellers and buyers. Sellers who provide owner financing can benefit from faster marketing time, additional profit from interest income, and spreading the payment of capital gains tax over a more extended period.

Buyers who buy property from a seller carrying the note can benefit from having flexible loan terms, a faster close of escrow, and lower loan fees since no commercial lender is involved in the transaction.

Source: What is Owner Financing for Commercial Property? | Crexi Insights

https://www.creconsult.net/market-trends/what-is-owner-financing-for-commercial-property/

Finding your next multifamily investment can be challenging, especially in today’s market environment. Cap rates are at record lows, and interest rates are rising. Inflation climbed 7.9% year-over-year as of February 2022, increasing operating expenses and the cost of capital improvements. Rent growth has been the only saving grace, surging nearly 20% across the top 50 metros in 2021.

Discovering the right opportunity requires looking at more deals when they hit the market and being prepared to move forward quickly with a firm bid. Understanding your financing options is vital for improving your chances of being awarded a deal and maximizing your returns.

When considering your financing options for 5+ unit multifamily properties, you should go beyond your local bank and consider financing through an agency small loan program. Fannie Mae Small Loans and Freddie Mac Small Balance Loans (SBL) offer some of the most competitive terms in the market, so they’re worth exploring if your property is eligible. This article will walk you through your financing options and help you navigate the property-specific agency small loan requirements, so you know what to look for when searching for your next multifamily investment.

Fannie Mae Small Loans and Freddie Mac Small Balance Loans (SBL) can be game changers for achieving your investment goals, limiting risk, and maximizing returns. They typically provide an ideal mix of low rates, maximum leverage, speed to close, and non-recourse debt for stabilized, 5+ unit multifamily properties. Specific benefits include:

| Financing options | Potential advantages | Typical disadvantages |

| Banks and credit unions | Floating rate options Less than 5-year loan terms available Shorter closing time frame Less stringent property and borrower requirements Lower prepayment penalties Less due diligence/ documentation Lower closing costs |

Higher rates Capped at 75% LTV Limit cash-out proceeds 25-year amortization 5–10-year maximum loan terms Limited interest-only Full or partial recourse Not assumable Limited geographically Deposit requirements Less stable source of capital |

| FHA/HUD | Lower rates Up to 35-year amortization and loan terms Construction and rehab loan products are also available |

Typically require 6+ months to close More excellent due diligence/ documentation No hybrid rate options |

| CMBS | Less stringent property and borrower requirements May allow the use of mezzanine debt or preferred equity |

Higher rates Capped at 75% LTV 10-year maximum loan term $2MM minimum loan amount Less flexible prepayment options Cannot hold rate until a few days before closing Less stable source of capital More stringent servicing requirements w/ cash management triggers |

| Life companies | Lower rates Rate locked at the application |

Capped at 65-70% LTV Limit cash-out proceeds Limited to higher-class properties 25-year amortization $2MM minimum loan amount |

| Debt funds, construction, bridge, and hard money lenders |

6-month to 3-year loan terms Do not require stabilized Occupancy (lend on new construction, lease-up, and rehabilitation/ redevelopment projects) Shortest closing time frame |

Higher rates and only floating rate options are available Capped at 75% LTV Shorter loan terms Partial or full recourse |

Local banks and credit unions may provide greater flexibility and lower closing costs, however; they will likely have higher rates and limit you to 75% LTV, 5-year loan terms, 25-year amortization, no interest-only, and require at least partial recourse.

Lenders that may be able to offer lower rates, such as FHA/HUD or life companies, require greater due diligence and can take too long to close (FHA/HUD) or are only available for higher class properties and limit your loan proceeds to less than 70% LTV (life companies).

So, what should you look for when searching for your next multifamily investment to ensure you can take advantage of the ideal mix of terms provided by Fannie Mae and Freddie Mac’s small loan programs?

A great place to start your property search is right here on Crexi! You can apply the following filters to make sure your property meets the agency programs’ “must-have” requirements:

And don’t forget to consider the other eligibility criteria as you narrow your search. Once you’ve identified a winning property and are ready for more precise loan terms based on your unique situation and goals, connect with one of our expert MultiFi partners to learn more and get a quote!

Source: How to Find and Finance Your Next Multifamily Property | Crexi Insights

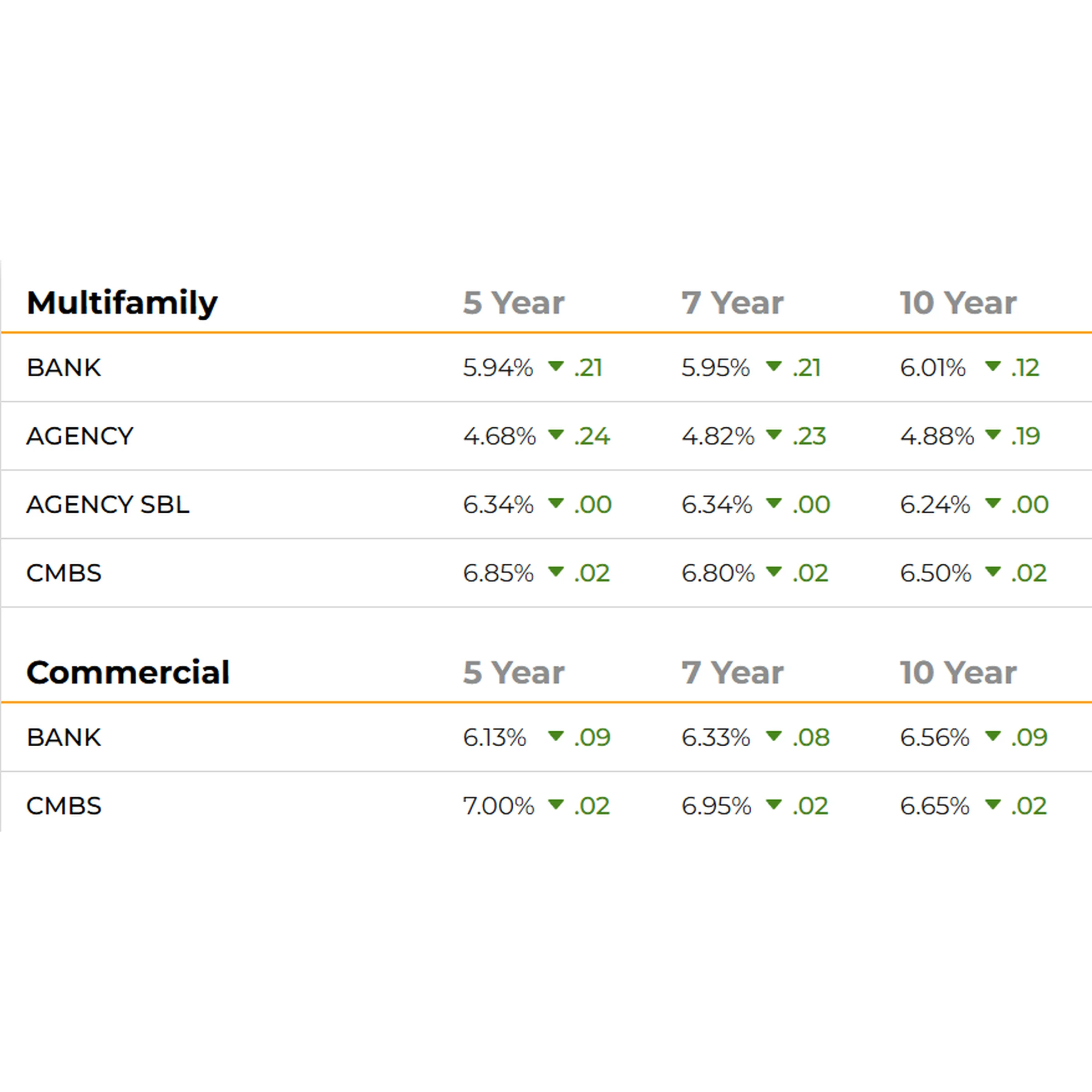

https://www.creconsult.net/market-trends/how-to-find-and-finance-your-next-multifamily-property/Stabilizing Debt Costs Create Tactical Opportunities for Apartment Owners Updated: February 2026 Chicago multifamily mortgage rates are stab...