In the face of economic uncertainties, timing the market for the acquisition (or disposition) of commercial real estate can be challenging. And while it’s been posited that market timers usually fail, acquisition price is crucial to investment success. An abundance of pessimistic voices insinuates adverse market outcomes, painting a grim picture of doom and gloom as we head into 2024. Social media and echo chambers can make these voices seem outsized, but many qualitative views and quantitative metrics indicate that those voices don’t tell the entire story.

Plenty of indicators suggest that if you have access to capital, commercial real estate may currently present a good buy opportunity. These, as well as real estate’s inherent and historic stability amidst fluctuating signals, suggest that those who stay levelheaded and key into signals within the noise may tap into significant potential returns.

There’s real distress, but trends are cyclical

Cycles occur and exist as an inevitable component of any investment sector. After 9/11, for example, some thought people would never work in high-rise office buildings again. Yet, until COVID-19 changed many of our norms, offices were a strong product type. The dot-com bubble, the savings and loan crisis, the global financial crisis—the commercial real estate sector swelled and compressed through each of these yet stood at nearly $4 trillion of total market value in 2022.

The psychology of markets propels these shifts: People swing from bullish to bearish and sometimes believe the pendulum will freeze until it inevitably moves again. The herd often thinks the good times and the bad times will never end while we are in them. Those who ignore the noise and zig while others are zagging can make fortunes.

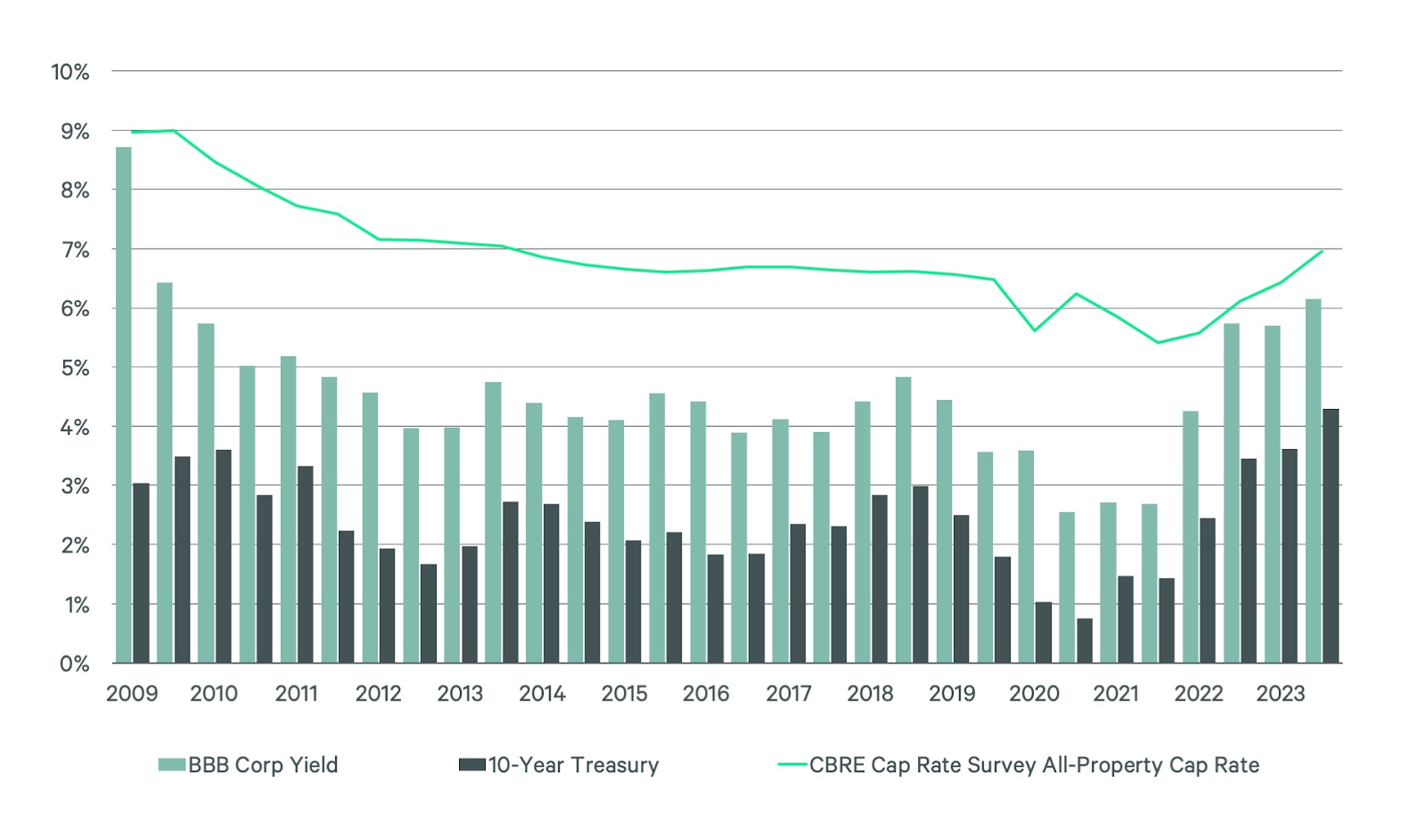

Much of today’s distress is driven by interest rate increases, but these rates are still historically low—just ask an investor from the 1980s, when rates were in the high teens. One can argue that several years of near-zero rates have bred complacency and that these rate hikes are calling on CRE stakeholders to level up to survive. It’s not easy money anymore, but that doesn’t diminish the sector’s potential.

This leveling up ultimately will make the overall sector much stronger, built on more well-crafted debt structures, invested in better value deals, and with a sharper-honed sense of the market’s cyclical reality.

There are asset class-specific and macroeconomic concerns that are worth mentioning. Global news has many on high alert as we watch developments in geopolitical conflicts and their economic impacts ripple through the U.S. economy. Inflation’s growth is slowing as of last month, yet our GDP continues to rise.

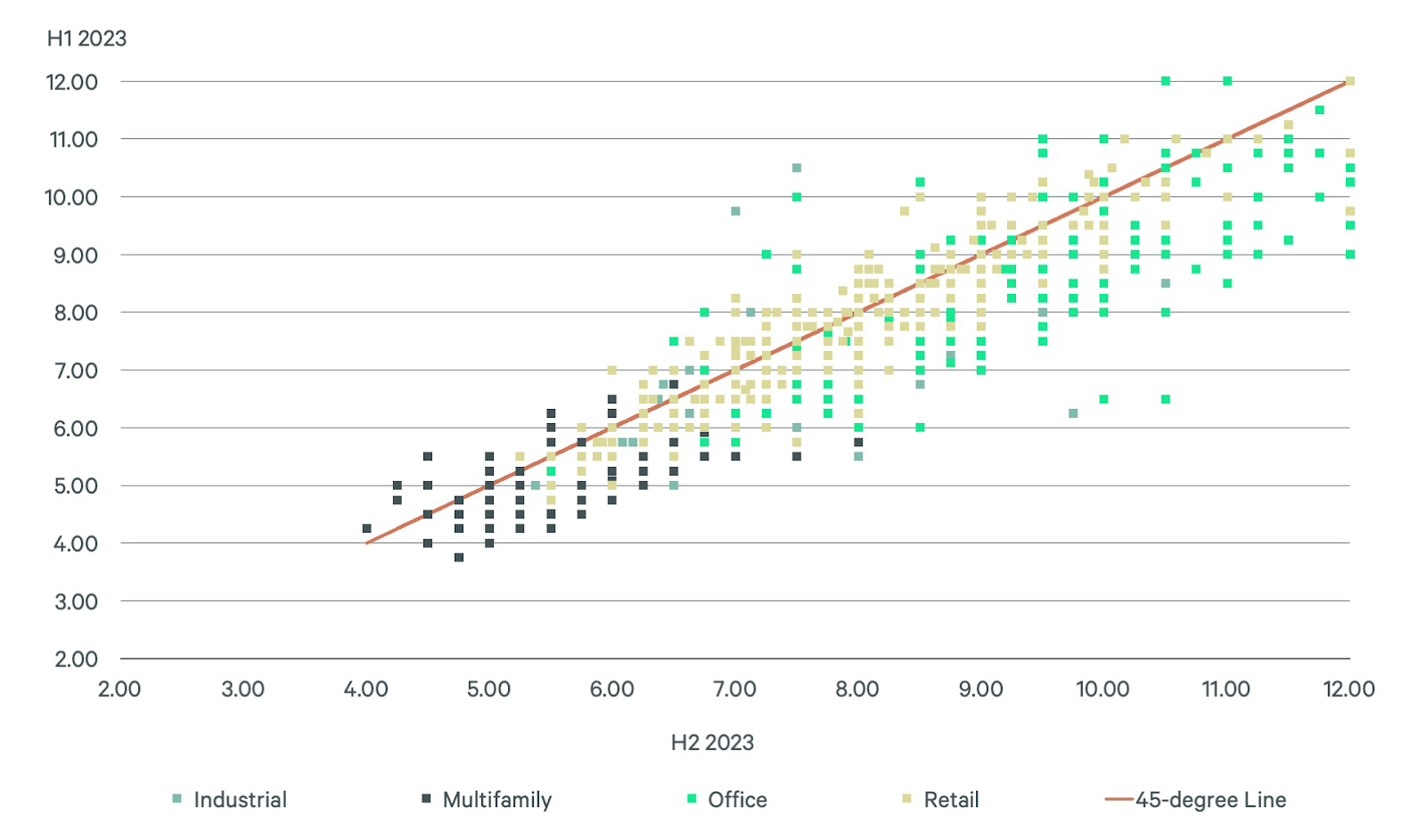

Offices are potentially nearing a trough, but there will likely be plentiful opportunities to acquire great assets at a discount for those who can source capital. If demand for space returns as companies call the herd back to the office (in some form), a lack of new office development may result in a shortage and a return to health or even prosperity. Retail and industrial sectors are relatively insulated despite potential shifts in consumer spending habits. Multifamily housing becomes ever more crucial as families get priced out of single-family homes.

Real estate’s inherent diversification proves immensely attractive in a world of fast-shifting share prices, exchanges escalating up and down, and meme stocks. Investing in commercial properties broadens your portfolio beyond the traditional forms of investments, like stocks and bonds, into the world of industrial, retail, and housing.

CRE is built on relationships

As any good broker or investor knows, the commercial real estate industry is built on relationships. During less free-flowing market phases, especially as we come off a long bull run, these relationships become ever more crucial.

Within this sector, CRE participants are making moves amid distress to creatively problem-solve refinancing issues, deal flow, and even landlord-tenant relationships. Banks and lenders, with an understanding that buildings are best retained and managed by more entrepreneurial borrowers, are motivated to meet owners at the bargaining table and come up with creative term adjustments and modifications. Especially as banks continue tightening their lending requirements overall, it’s essential to build up these good relationships now and reaffirm a commitment to mutual success.

While buyers are taking longer to source, evaluate, and close deals, they’re much better prepared to take advantage of good opportunities when they appear if they’ve cultivated fruitful relationships with brokers, financiers, and other key transaction personnel. Many, indeed, are assembling such networks and keeping a close eye on market trends to strike when the iron’s most hot.

Landlords, too, are engaging in ongoing conversations with prospective and current tenants, especially those with upcoming lease renewals. By keeping these dialogue channels open, tenants get more attractive lease terms, while landlords can rest assured of their rent payments. Happy tenants are much likelier to stick around for the long haul—a reassuring guarantee of stable cash flow amid more volatile markets.

Strong careers are forged in tough times

What’s different this time around? New tech tools and broader access to democratized information are unlocking efficiency and potential more than ever, making now an exciting, if challenging, time to enter and stay in commercial real estate.

Advanced digital marketing tools not only widen the reach of a listing to prospective buyers or tenants but also provide detailed insights into who that audience pool is or even could be. More and more brokers are adopting digital listing platforms, social media, and advanced CMS software to establish and nurture client relationships. Outside of a particular deal, these relationship tracking tools facilitate relationship building, which, as mentioned above, is crucial to the industry’s success.

The integration of big data and analytics is also transforming the way commercial real estate operators make decisions. The aggregation of data such as market trends, demographic shifts, sales comparables, and foot traffic makes holistic due diligence faster, more transparent, and fully remote if need be. There’s a hunger for information and better tools, and advances in AI and other technological sectors allow CRE stakeholders to prioritize relationship-building while automating other facets of their business.

Additionally, predictive analytics tools can help identify emerging trends, forecast demand, and assess the potential profitability of a given asset. This level of analysis was previously time-consuming and costly, but with advancements in research tools, investors can now access comprehensive data and analytics tools, giving them a competitive edge in the market.

New technologies are also making engagement with mentors and industry leaders more accessible than ever, through articles, education, and even DMs. Advances in digital marketing tools have dramatically reduced business costs, and it’s never been easier to build a unique brand and highlight what differentiates you as an investor, landlord, or broker. Using technology well can offer savvy CRE stakeholders a distinct advantage.

Outside of technological advancements, an environment of adversity breeds resilience. Many Crexi Podcast guests acknowledge current challenges but claim there’s never been a better time to enter the sector, as troubles sharpen skills, strengthen networks, and demonstrate one’s capabilities. Younger professionals are also excited about the chance to prove themselves in a shifting market, and those who become exposed early on to the potential financial hurdles of a CRE-focused career will be better equipped to thrive when the tides shift.

The bottom line

Real estate remains one of the best asset classes and ways to maintain control of your money’s destiny. Those with entrepreneurial grit who can best prepare themselves, increase their knowledge, optimize their toolkit, and develop relationships will be best positioned when the wheel of fortune turns back around.

Request a consultation to explore how our network can unlock CRE opportunities for you.

Source: The sky isn’t falling. Here’s why we remain bullish on CRE

https://www.creconsult.net/market-trends/cre-investment-strategies-2024/