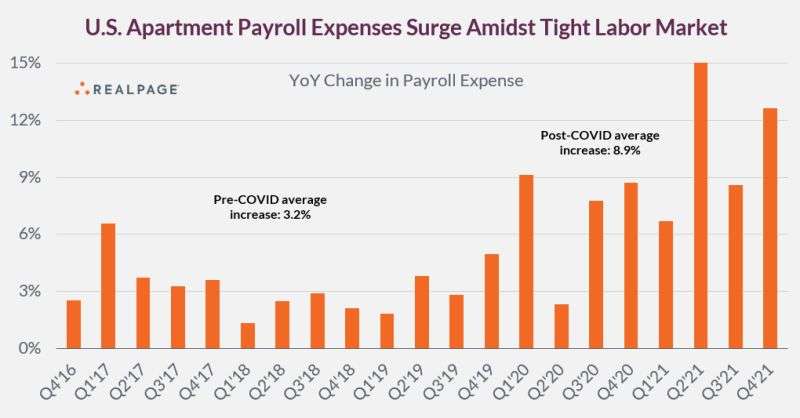

While rents grow at an unprecedented pace, so do payrolls. Apartment operators are fighting to retain and hire talent, and that's a win for community managers, leasing agents, and maintenance technicians. Apartment payrolls have surged by 12.6% in 2021 -- lifting the average increase in the COVID-era to 8.9%. By comparison, payrolls grew by an average of 3.2% annually pre-COVID.

Property management is certainly not unique in that regard. For all the (much warranted) talk about inflation, it's often lost that WAGE GROWTH plays a key role in inflation. Businesses are spending more on their top asset -- their people. And while salaries do not necessary keep pace with costs for every worker in every sector, most apartment staff are likely seeing wage growth above the national norms. We're hearing all the time how much property managers are fighting for talent. Your competitors are trying to lure away your best people. You're sometimes pulling from hospitability sectors to find potential leasing agents with no direct industry experience. And you're doing all you can to incentivize your best people to stay. Pay is a big piece of it, but not the only piece. It's also work/life balance and job duties -- relying more on technology and centralization to free up your on-site teams to focus on the highest-value tasks: leasing out units and taking care of residents. On-site teams are people/people ... this is what they want to do. Back-office work is burnout work.Many property management companies are also operating with fewer people on-site, but that makes those remaining roles all the more valuable (and more expensive).

Source: https://www.linkedin.com/posts/jay-parsons-a7a6656_propertymanagement-apartments-wages-activity-6909501365589319680-1QiQ?utm_source=linkedin_share&utm_medium=member_desktop_web