Tuesday, September 27, 2022

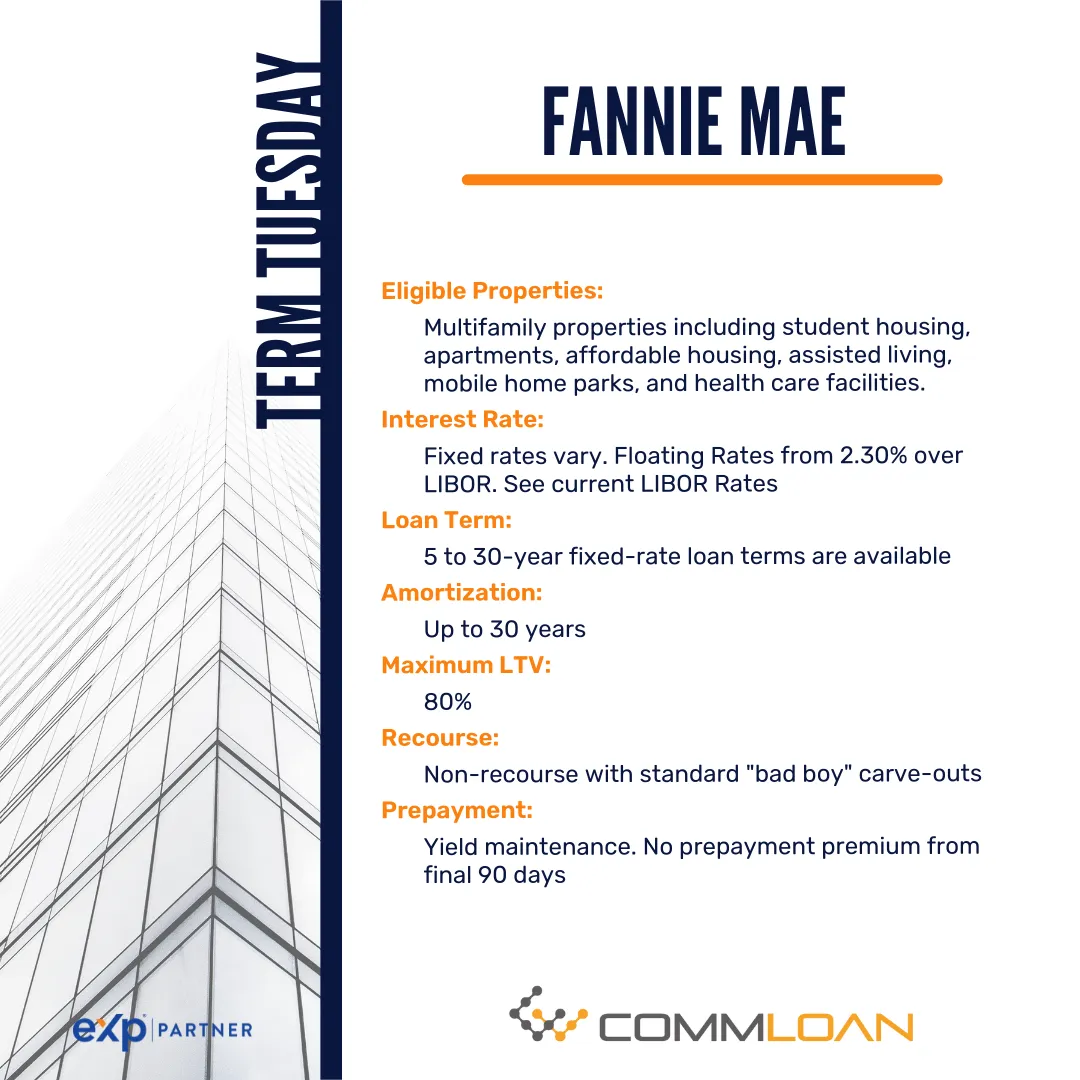

Term Tuesday: Fannie Mae. For commercial real estate investors, #FannieMae #Multifamily #loans may prove to be a feasible way of obtaining lower costing financing. It is one of the largest sources of capital within this market in the U.S.

View our Guide to Multifamily Real Estate Loans and obtain quotes from hundreds of lenders from eXp Commercial's National Capital Markets Partner CommLoan. The Largest Commercial Real-Estate Lending Marketplace.

https://www.creconsult.net/market-trends/guide-to-commercial-multifamily-real-estate-loans/

Monday, September 26, 2022

5 Incentives to Increase Multifamily Lease Renewals

Resident retention remains a high priority, and these five incentives can help earn renewals.

5 Incentives to Increase Multifamily Lease Renewals -

It costs a whopping $3,976 to replace one of your residents when they don’t renew their lease, which is up from $3,850 last year, according to Zego’s “The 2022 State of Resident Experience Management Report.”

One of the most valuable assets to any apartment manager is current residents and, as such, resident retention should be one of the highest priorities. To do that, you need exciting apartment renewal incentives to remain competitive. Here are five renewal incentives to try:

1. Free Apartment Upgrade

While it may not be possible to avoid increasing rents in the community, one way to incentivize residents to renew their leases is by offering more value. That value could be presented as an apartment upgrade for the same rate or at a discounted rate from their current apartment.

The upgrade does not always have to be a larger apartment, it could be in a better location at the property or one that includes an in-unit washer/dryers and a balcony or patio. And if you don’t have any available upgrades, you can offer to improve your resident’s current apartment as an incentive. For example, upgrading the appliances is a great way to elevate the apartment and even justify a rent increase.

2. Resident Events

According to Satisfacts, resident events are one of the significant drivers of lease renewals. Resident events can help establish stronger connections and relationships between residents, which can improve a community’s turnover rate.

However, planning a successful resident event is much easier said than done — especially for the busy multifamily marketing professional.

Here are a few resident event ideas:

3. Free Month of Rent

Once you lose a resident, that means you have to start over by building trust and a relationship with the new resident.

Consider incentivizing your best residents because one significant reason someone might not renew their lease is financial concerns. A free or discount on their first month’s rent could mitigate those worries.

4. Invest in Smart Locks

While you can never promise 100% safety and security anywhere, you still want your residents to feel safe and relaxed in their homes. Upgrading your property with smart locks or controlled, gated access can offer them peace of mind (and justify a rent increase, if needed).

5. Concierge Services

Residents value convenience any way they can get it. From partnering with dry cleaners or grocery delivery apps, there are many ways to offer concierge-style services at the community. These added services can help incentivize renewals as well as justify a rent increase, especially if you add multiple services.

For example, consider integrating convenience or property management apps on a resource page on your website, along with discount codes to use the services. Millennials and Gen Z are accustomed to these mobile conveniences, and there’s no reason their multifamily property can’t offer the same.

Add Convenience and Value to Earn Renewals

Ultimately, when it comes to resident retention, convenience is key. Moving out of an apartment is stressful. Nobody wants to move if they can avoid it; avoid providing a reason for residents to not renew their lease. If it’s more convenient for your residents to stay in their apartment, then they will, but it’s up to the property team to earn that renewal.

Source: 5 Incentives to Increase Multifamily Lease Renewals

https://www.creconsult.net/market-trends/5-incentives-to-increase-multifamily-lease-renewals/Sunday, September 25, 2022

Higher-Income Renters Pay the Biggest Rent Hikes and are Least Likely to Miss a Rent Payment

Here’s one of the most widely misunderstood realities of rental affordability: The renters seeing the largest rent hikes are upper-income households in the most expensive rentals, and despite larger rent increases, they’re least likely to miss a rent payment.

On the flip side, rent payments have fallen the most in subsidized affordable housing – where rents have grown the least, since those rents are typically set to a share of income.

So it’s not all about the rent, clearly. Yes, rent growth is a big part of the equation. But its impact tends to be mischaracterized and overstated.

The average renter in market-rate Class A and B units has seen rents increase 14 to 15% since March 2020, according to RealPage Market Analytics. (These are actual in-place rents, not asking rents.) Those renters are paying 96% to 97% of the rent due each month, which is off 1 percentage point from pre-COVID levels.

Why are these renters able to keep paying higher rents at essentially normal levels? Well, it all comes back to income. Class A and B renter households have seen incomes rise nearly as fast as rent (among new lease signers, where income is tracked at signing). A typical Class A renter household (including roommates) now has annual income of $135,000, while a typical Class B renter household is $99,600.

It’s a different story in Class C, also sometimes called “workforce housing.” Household incomes in Class C have grown, too, but annual wages remain lower at $62,000. While Class C in-place rents grew a lesser (but still significant) 10% since March 2020, we’ve seen a bit more distress in this group. Class C rent collections were lower than Class A and B pre-COVID, and that gap has widened a bit more since COVID hit.

And it’s even more challenging in the subsidized Affordable Housing space. Affordable housing typically locks the rent at a level relative to income (specific programs can vary). But that rent stability hasn’t been enough to help all Affordable renters. In fact, rent collections have fallen about 4 percentage points since COVID hit to just under 87%.

Three Takeaways:

1) Renters in Class C and Affordable are most price sensitive, but it’s not all about the rent. When other consumer costs skyrocket (like groceries, up 13%), there’s less money available to pay rent for some households.

2) Renters making the highest incomes tend to pay the largest rent increases. This is why it’s SO CRITICAL to segment the rental market. Too many pundits paint it with a very broad brush that distorts the facts around rental affordability.

3) No matter how you slice it, actual rent collections are significantly higher than what the experimental and tiny Census Household Pulse Survey is showing. The Census itself warns that their rent payment surveys have major statistical holes, yet those warnings are routinely disregarded by those who use their data.

What Does This Mean for the Road Ahead?

Despite headlines to the contrary, rental affordability has been more of a tailwind than a headwind – particularly for the market-rate, professionally managed rental housing sector. We detailed rental affordability in depth in a study released in July examining rents and incomes from 7 million leases – the largest-ever study on rental affordability. In the report, we noted some of the reasons why market-rate renters have outperformed the government’s national averages for wage growth.

But the road ahead is less clear. Rent growth is mitigating to more normal levels. Resident retention rates are moderating back down from all-time highs. Rising mortgage rates, contrary to conventional wisdom, are not boosting demand for rentals. In fact, we’re on track to record net absorption well below the record peaks of 2021 (though still at healthy levels). And eroding consumer sentiment amidst inflation appears to be eating away at household formation and housing demand.

On the positive side, job growth remains strong in most markets – and unemployment very low. Those are strong tailwinds for continued wage growth.

In any scenario, though, it’s unlikely renters will face anything like the COVID-era lockdowns that resulted in 20 million job losses. Even then, rent collections held up much better than expected – long before stimulus and rental assistance programs kicked in (which helped later on). And while consumer costs are much higher now due to inflation, that recent history of renter resilience is a good indicator should the economy sputter again.

Source: Higher-Income Renters Pay the Biggest Rent Hikes and are Least Likely to Miss a Rent Payment

https://www.creconsult.net/market-trends/higher-income-renters-pay-the-biggest-rent-hikes-and-are-least-likely-to-miss-a-rent-payment/Saturday, September 24, 2022

HUD Announces Increased Payment Standards, More Vouchers | National Apartment Association

On September 1, 2022, the U.S. Department of Housing and Urban Development (HUD) released its updated fair market rents (FMRs) for fiscal year 2023. Each year, HUD updates the FMRs to, among other things, set a reasonable payment standard for public housing agency (PHA) payments to housing providers participating in the Section 8 Housing Choice Voucher (HCV) program. Nationally, the average FMR increased by about 10 percent.

This update to payment standards comes at a critical time when pandemic recovery, inflationary pressures, and the massive housing shortage have forced average rents up across the country. For example, FMRs in Phoenix will increase by 33 percent in response to significant demand.

“These new FMRs will make it easier for voucher holders facing this challenge to access affordable housing in most housing markets while expanding the range of housing opportunities available to households,” said HUD Secretary Marcia Fudge in a press release.

Here are some of the key takeaways from the announcement.

New Data sources

Typically, HUD utilizes the Census Bureau’s American Community Survey (ACS) to estimate the 40th percentile gross rents of households that recently moved into an area. This often provides an accurate picture of near-median rents for new leases. Last year, however, the Census Bureau announced that it would not release the estimates from the 2020 ACS because the COVID-19 pandemic had interfered with data collection. Instead, HUD supplemented private market data to maintain the accuracy of the FMRs, sourcing data from RealPage, Moody’s Analytics, CoStar Group, CoreLogic, Apartment List and Zillow, as examples. Industry groups, including NAA, raised concerns about the use of this data. Using private data precludes stakeholders from checking to see if the data are consistent across time and location, and if they are representative of the population in question rather than collected based on the company’s anticipated ability to sell them. HUD is expected to use solely once again the ACS data in the following years.New Vouchers

In addition to higher rates, HUD will award approximately 19,700 new Housing Choice Vouchers to PHAs. This increase is made available by the Consolidated Appropriations Act of 2022 which was signed into law on March 15, 2022. HUD has sent a notification to eligible PHAs informing them of the new vouchers providing a deadline of September 2 to accept or decline the increase.Policy Outlook

The National Apartment Association (NAA) urges policymakers to adopt responsible and sustainable housing policies. Additional vouchers and FMR increases are desperately needed for low- and moderate-income households and housing providers who have been thrust into financial uncertainty amid economic turmoil due to the pandemic. Nevertheless, there is more to be done. The HCV Program is fraught with payment delays, impractical inspection requirements and administrative red tape which makes housing provider participation infeasible in countless markets. To help address the industry’s concerns, NAA continue to prioritize and encourage support for the Choice in Affordable Housing Act (S. 1820/H.R. 6880), introduced by Senators Chris Coons (D-DE) and Kevin Cramer (R-ND) in the Senate, and by Representatives Emmanuel Cleaver (D-MO-05) and John Katko (R-NY-24) in the House. NAA worked closely with the bill’s sponsors to include several industry priorities, which were formulated with NAA member feedback, in the legislation to speed up tenancy approval processes, reduce duplicative inspections requirements and provide better ongoing support for housing provider participants. We look forward to continuing this work with Congress and the Administration to advance the industry’s advocacy goals and responsibly and sustainably address the nation’s housing affordability challenges. For more information on Housing Choice Voucher Program policy, please contact Ben Harrold, NAA’s Manager of Public Policy.Source: HUD Announces Increased Payment Standards, More Vouchers | National Apartment Association

https://www.creconsult.net/market-trends/hud-announces-increased-payment-standards-more-vouchers-national-apartment-association/Friday, September 23, 2022

An Inflection Point for Multifamily Lending - Freddie Mac

Freddie Mac, and agency lending in general, has been foundational to the success of the multifamily industry in the post-Great Recession era. Prior to our more active role in the financing of rental housing, the market lacked stability and liquidity throughout the cycle. Workforce and Targeted Affordable Housing were particularly deficient and inconsistent sources of debt. Today we lead the industry in this highly affordable space where we lend expertise in addition to capital.

At no time was this truer than in our response to the pandemic housing market. Fulfilling our countercyclical role, we stayed on the field as many capital sources moved to the sidelines. The result was a debt market that continued to perform efficiently. Multifamily transactions never stopped, and borrowers benefited from a historically low-rate environment. Freddie Mac and Fannie Mae also extended unprecedented flexibility to borrowers and essential protections to tenants in a way that no other debt capital sources could.

As the economy recovered from the pandemic, multifamily housing demand accelerated, vacancies cratered, and rents shot up like nothing we have ever seen before. There are a host of reasons why this happened. A long-run housing supply shortage that predates COVID-19 worsened as a result of pandemic-related supply chain issues, labor shortages, and construction delays. A highly competitive single-family market drove more households to become or remain renters. The desire for more personal space caused roommates to seek solo accommodations. Remote work enabled office workers to relocate. Certainly not least, higher salaries and inflation shifted the demand curve.

We saw big changes on the supply side too. Investor interest in multifamily throughout the capital stack jumped markedly. In a world of economic uncertainty, multifamily is a proven, reliable asset class and an inflation hedge to boot. With rising net operating incomes and values, it has been the place to be for many investors. This surge in capital has also driven new construction – an excellent signal that supply has room to grow even if never fast enough.

Today we’re at something of an inflection point. Inflation risk and recession fears have many debt providers tightening or closing up. At the same time, we have a negative leverage issue with note rates catching up to, and in some cases surpassing, cap rates which have been trending down for some time. Fewer deals seem to pencil in as interest rates surpass investment returns. As a result, the market is in a period of transition.

The fundamentals, however, are very strong, and lenders that maintained credit discipline and appropriately distributed risk are well positioned to weather even a serious economic downturn.

Freddie Mac Multifamily counts itself among those market participants and stands ready to continue deploying capital consistently and responsibly. We’ll do this, as always, in a way that is mission-centric. That’s more important than ever, given the essential role we play in helping address the housing affordability crisis.

The current economic moment is accelerating the need for action. Freddie Mac recently fielded a survey that shows 58% of renters have seen their rent increase in the past 12 months. Although salaries are on the rise, a third of renters say their rent increase was greater than any raise they received at work. More concerning is that nearly 20% say that their rent increase makes them extremely likely to miss a rent payment.

To address the affordability crisis, we are driving toward a record year for our Targeted Affordable Housing business, and we’re poised to meet our aggressive affordability goals. This year, at least 50% of our production volume must support units that are affordable to families earning 80% of area median income (AMI) and 25% must support units affordable at 60% AMI. We said at the beginning of the year that this would be a tough challenge, but that we are up for the task. We’ve prioritized our mission-driven business.

Separately, we recently announced a landmark Equitable Housing Finance Plan that proposes several new initiatives aimed at enhancing borrower diversity, advancing tenant interests, and broadly addressing affordability through both preservation of and support for new supply. Building on past efforts, we’ve also expanded our Duty to Serve commitments to address housing needs in underserved markets, including rural communities and manufactured housing communities.

We know there is tremendous work to be done to ensure that more Americans can find safe and affordable rental housing, and as the new head of Freddie Mac Multifamily, it’s my highest priority. As the market dynamic shifts, we will continue to ensure a stable foundation for the multifamily industry while seeking out new innovations that can make homes possible for more of the nation’s 44 million renting households.

Thursday, September 22, 2022

LIVING COST SENSITIVITY AND SLOWER HOUSEHOLD CREATION MODIFY DEMAND FLOWS

The sequence of rate hikes decay housing affordability. In late July, the Federal Reserve again lifted the overnight rate by 75 basis points to a target range of 2.25 to 2.50 percent. This will likely apply additional upward pressure to mortgage rates, with the 30-year fixed rate already climbing more than 200 basis points this year to 5.3 percent at the end of July. Higher borrowing costs amid towering home prices make ownership difficult for a growing share of the population. As of June, the estimated affordability gap, or the difference between a monthly payment on a median-priced home and a rent obligation, in the U.S. surpassed $1,000. That margin was about half as large just 12 months earlier, demonstrating how the relative affordability of apartments is improving, despite robust rent growth. For some markets, however, higher home and rent costs amid inflation is slowing demand.

Demand cools in some pandemic-era darlings. Both the number of homes sold and apartment units absorbed fell in the second quarter, a signal that household formation may be moderating. This contraction occurred during the same three-month span in which more than 1.1 million jobs were added, a process that typically supplies residents with incomes and the stability to form households. More renters are likely opting for roommates or moving back in with family. These trends are most evident in the secondary and tertiary metros in the Sun Belt that led the nation in net absorption during 2021. After such a heated pace, this cooling of demand is giving supply a chance to catch up.

Resident bases are reshuffling. Among the 30 U.S. metros that topped the nation in net apartment absorption during the second quarter, about half had an average effective rent at least 25 percent below the national mean. Places such as Huntsville — situated within 200 miles of Nashville and Atlanta — recorded their highest quarterly absorption on record. Lower-income residents priced out of larger metros in the region, and migrating households seeking less costly living options with proximity to bigger cities may be moving in. Relatively affordable Midwest metros like Madison, Omaha, and Des Moines also had a strong second quarter.

Developing Trends

Household creation may be hindered in the second half. Coming off a record year in 2021 when more than 1.3 million new U.S. households were formed, a near-term slowdown is materializing. Approximately 85,000 fewer households were created during the first half of 2022 compared to the same six months of last year. The housing shortage contributed to this, as a lack of available homes and rentals kept some young adults living at home or in roommate situations. Rental vacancy and single-family home listings remain very low, enforcing a persistent constraint on household formation. In the coming months, economic headwinds and growing affordability challenges could inhibit young adults’ ability to find jobs and willingness to move out on their own.

The streak of monthly home price rises ends. The median sale price of an existing home fell 1 percent month-over-month in June, the first reduction since mid-2020. Sellers are adapting to the new environment, with purchase activity down almost 13 percent year-over-year. Even with the abatement, the median cost held above $400,000 in June, up 39 percent since the onset of the pandemic.

16.9% |

38.0% |

| Year-Over-Year Change in Average Effective Apartment Rent | Year-Over-Year Change in Average Monthly Mortgage Payment |

* Through 2Q Sources: Marcus & Millichap Research Services; Capital Economics; Freddie Mac; Moody’s Analytics; Mortgage Bankers Association; National Association of Home Builders; National Association of Realtors; RealPage, Inc.; Redfin; U.S. Bureau of Labor Statistics; U.S. Census Bureau; Wells Fargo

Wednesday, September 21, 2022

Chicago Multifamily Market Report

Chicago Multifamily Market Report

2Q 2022

Demand Returns to Central Neighborhoods; Suburban Apartment Market Maintains Strength

Absorption in urban locales accelerates. Due to space constraints in the urban core, new supply has been and will continue to be limited in the core this year. This has produced historically tight conditions in many central neighborhoods, as construction in the core has been unable to match renter demand. Preliminary data shows a 440-basis-point annual drop in vacancy within Chicago proper at the end of March. Competition for units here is likely to result in sharp rent climbs this year, especially in locales like Lincoln Park, Ukrainian Village, and Andersonville. Also, the return to in-person work downtown supported near nation-leading annual vacancy contraction in The Loop and West Loop areas entering the second quarter. This tightness may spur more development in central locales in future years.

Subscribe to:

Posts (Atom)

-

Just Listed: Golf Sumac Medical Offices | Des Plaines IL Price: $3,900,000 SF: 35,245 Stories: 3 Occupancy: 82.3% Cap Rate: 9.63% * Stabiliz...

-

🏢 Two Adjacent Turnkey Office Buildings For Sale – Joliet, IL 🏢 Located just off Larkin Ave and adjacent to Ascension St. Joseph Medical C...

-

Introduction The Kane County multifamily market in Q3 2024 offers solid opportunities for investors and property owners. As one of the most...